Southampton-3

not in an election year for sure.................................

Join Date: Nov 2015

Location: Southampton

Posts: 632

Likes: 0

Received 0 Likes

on

0 Posts

Join Date: Apr 2018

Location: UK

Posts: 538

Likes: 0

Received 0 Likes

on

0 Posts

Join Date: May 2009

Location: Southampton, U.K

Posts: 1,265

Likes: 0

Received 0 Likes

on

0 Posts

S24 Summary

Usual summary of routes for S24. I've generally looked at early April and mid August to get a rough idea of the frequency variations. Good to see Aer Lingus increase frequencies from June, I think the overall capacity to Belfast now exceeds what Flybe used to offer on the route. Overall it is a little lower in departures than last year, but most of the increased frequencies are on larger aircraft which should more than make up for the difference in capacity terms.

Aer Lingus Regional

Belfast City - 13-20 weekly AT7

Dublin - 13-14 weekly AT7

Aurigny

Alderney - 14 weekly D28

Guernsey - 7 weekly AT7

BA Cityflyer

Bergerac - 1 weekly E90

Faro - 1 weekly E90

Malaga - 1 weekly E90

Palma - 1 weekly E90

Blue Islands

Guernsey - 16 weekly AT7

Jersey - 22 weekly AT7

Eastern Airways

Paris CDG (New) - 6 weekly AT7 (from 01/04)

easyJet

Alicante (New) - 1 weekly 319 (from 31/03)

Belfast International - 5 weekly 319/320

Faro (New) - 1 weekly 320 (from 06/06)

Glasgow - 2-7 weekly 319/320

Palma (New) - 2 weekly 319/320 (from 29/04)

KLM

Amsterdam - 13-20 weekly E75/E90

Loganair

Edinburgh - 21-26 weekly ER4

Glasgow - 18-21 weekly ER4

Newcastle - 13-15 weekly ER4

TUI

Palma - 2 weekly E90 (operated by BA Cityflyer)

Summary

171-195 weekly departures (up to 199 in S23, 321-344 in S19)

24-28 average daily departures (up to 28 in S23, 46-49 in S19)

Aer Lingus Regional

Belfast City - 13-20 weekly AT7

Dublin - 13-14 weekly AT7

Aurigny

Alderney - 14 weekly D28

Guernsey - 7 weekly AT7

BA Cityflyer

Bergerac - 1 weekly E90

Faro - 1 weekly E90

Malaga - 1 weekly E90

Palma - 1 weekly E90

Blue Islands

Guernsey - 16 weekly AT7

Jersey - 22 weekly AT7

Eastern Airways

Paris CDG (New) - 6 weekly AT7 (from 01/04)

easyJet

Alicante (New) - 1 weekly 319 (from 31/03)

Belfast International - 5 weekly 319/320

Faro (New) - 1 weekly 320 (from 06/06)

Glasgow - 2-7 weekly 319/320

Palma (New) - 2 weekly 319/320 (from 29/04)

KLM

Amsterdam - 13-20 weekly E75/E90

Loganair

Edinburgh - 21-26 weekly ER4

Glasgow - 18-21 weekly ER4

Newcastle - 13-15 weekly ER4

TUI

Palma - 2 weekly E90 (operated by BA Cityflyer)

Summary

171-195 weekly departures (up to 199 in S23, 321-344 in S19)

24-28 average daily departures (up to 28 in S23, 46-49 in S19)

Join Date: Nov 2015

Location: Southampton

Posts: 632

Likes: 0

Received 0 Likes

on

0 Posts

Usual summary of routes for S24. I've generally looked at early April and mid August to get a rough idea of the frequency variations. Good to see Aer Lingus increase frequencies from June, I think the overall capacity to Belfast now exceeds what Flybe used to offer on the route. Overall it is a little lower in departures than last year, but most of the increased frequencies are on larger aircraft which should more than make up for the difference in capacity terms.

Aer Lingus Regional

Belfast City - 13-20 weekly AT7

Dublin - 13-14 weekly AT7

Aurigny

Alderney - 14 weekly D28

Guernsey - 7 weekly AT7

BA Cityflyer

Bergerac - 1 weekly E90

Faro - 1 weekly E90

Malaga - 1 weekly E90

Palma - 1 weekly E90

Blue Islands

Guernsey - 16 weekly AT7

Jersey - 22 weekly AT7

Eastern Airways

Paris CDG (New) - 6 weekly AT7 (from 01/04)

easyJet

Alicante (New) - 1 weekly 319 (from 31/03)

Belfast International - 5 weekly 319/320

Faro (New) - 1 weekly 320 (from 06/06)

Glasgow - 2-7 weekly 319/320

Palma (New) - 2 weekly 319/320 (from 29/04)

KLM

Amsterdam - 13-20 weekly E75/E90

Loganair

Edinburgh - 21-26 weekly ER4

Glasgow - 18-21 weekly ER4

Newcastle - 13-15 weekly ER4

TUI

Palma - 2 weekly E90 (operated by BA Cityflyer)

Summary

171-195 weekly departures (up to 199 in S23, 321-344 in S19)

24-28 average daily departures (up to 28 in S23, 46-49 in S19)

Aer Lingus Regional

Belfast City - 13-20 weekly AT7

Dublin - 13-14 weekly AT7

Aurigny

Alderney - 14 weekly D28

Guernsey - 7 weekly AT7

BA Cityflyer

Bergerac - 1 weekly E90

Faro - 1 weekly E90

Malaga - 1 weekly E90

Palma - 1 weekly E90

Blue Islands

Guernsey - 16 weekly AT7

Jersey - 22 weekly AT7

Eastern Airways

Paris CDG (New) - 6 weekly AT7 (from 01/04)

easyJet

Alicante (New) - 1 weekly 319 (from 31/03)

Belfast International - 5 weekly 319/320

Faro (New) - 1 weekly 320 (from 06/06)

Glasgow - 2-7 weekly 319/320

Palma (New) - 2 weekly 319/320 (from 29/04)

KLM

Amsterdam - 13-20 weekly E75/E90

Loganair

Edinburgh - 21-26 weekly ER4

Glasgow - 18-21 weekly ER4

Newcastle - 13-15 weekly ER4

TUI

Palma - 2 weekly E90 (operated by BA Cityflyer)

Summary

171-195 weekly departures (up to 199 in S23, 321-344 in S19)

24-28 average daily departures (up to 28 in S23, 46-49 in S19)

Join Date: Dec 2022

Location: UK

Posts: 205

Likes: 0

Received 0 Likes

on

0 Posts

Join Date: Nov 2014

Location: London

Posts: 491

Likes: 0

Received 0 Likes

on

0 Posts

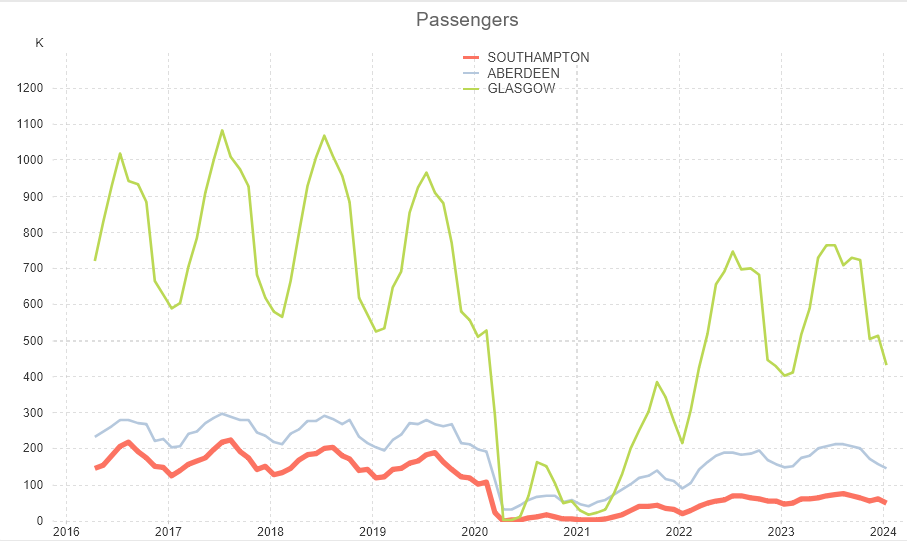

Southampton 12 month running total was 755,000 in Dec and has only moved marginally to 758k in January 2024. It will need to move significantly in April-October to ensure it get's to 900,000 but I doubt it will go above 950,000 for the year.

With easyJet reducing frequency on Belfast & Glasgow-Southampton back to thrice/twice weekly in the winter, that will be a large passenger shortfall in this calendar yr.

With easyJet reducing frequency on Belfast & Glasgow-Southampton back to thrice/twice weekly in the winter, that will be a large passenger shortfall in this calendar yr.

Join Date: Nov 2015

Location: Southampton

Posts: 632

Likes: 0

Received 0 Likes

on

0 Posts

Southampton 12 month running total was 755,000 in Dec and has only moved marginally to 758k in January 2024. It will need to move significantly in April-October to ensure it get's to 900,000 but I doubt it will go above 950,000 for the year.

With easyJet reducing frequency on Belfast & Glasgow-Southampton back to thrice/twice weekly in the winter, that will be a large passenger shortfall in this calendar yr.

With easyJet reducing frequency on Belfast & Glasgow-Southampton back to thrice/twice weekly in the winter, that will be a large passenger shortfall in this calendar yr.

Join Date: Jun 2012

Location: N.Ireland

Posts: 1,753

Likes: 0

Received 0 Likes

on

0 Posts

Southampton 12 month running total was 755,000 in Dec and has only moved marginally to 758k in January 2024. It will need to move significantly in April-October to ensure it get's to 900,000 but I doubt it will go above 950,000 for the year.

With easyJet reducing frequency on Belfast & Glasgow-Southampton back to thrice/twice weekly in the winter, that will be a large passenger shortfall in this calendar yr.

With easyJet reducing frequency on Belfast & Glasgow-Southampton back to thrice/twice weekly in the winter, that will be a large passenger shortfall in this calendar yr.

Join Date: Mar 2004

Location: Dorset

Posts: 677

Likes: 0

Received 0 Likes

on

0 Posts

Based on the CAA numbers earlier in the thread, this isn�t looking great. The rolling annual pax figures should be showing some half decent upward trend if the easyJet BFS and GLA flights are truly creating a new market. They�re nearly static which says loud and clear that all easyJet has done so far is cannibalise passenger numbers from existing operators, exactly as I had feared.

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

Based on the CAA numbers earlier in the thread, this isn�t looking great. The rolling annual pax figures should be showing some half decent upward trend if the easyJet BFS and GLA flights are truly creating a new market. They�re nearly static which says loud and clear that all easyJet has done so far is cannibalise passenger numbers from existing operators, exactly as I had feared.

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

Really its very early days for any verdict on the runway extension. Two years down the line and the wisdom or otherwise will become clearer. Hopefully the owners are playing the long game.

Join Date: Nov 2015

Location: Southampton

Posts: 632

Likes: 0

Received 0 Likes

on

0 Posts

Based on the CAA numbers earlier in the thread, this isn’t looking great. The rolling annual pax figures should be showing some half decent upward trend if the easyJet BFS and GLA flights are truly creating a new market. They’re nearly static which says loud and clear that all easyJet has done so far is cannibalise passenger numbers from existing operators, exactly as I had feared.

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

Join Date: Dec 2023

Location: Southampton

Posts: 48

Likes: 0

Received 0 Likes

on

0 Posts

It's really much too early to be gloomy; no one can tell what 2024 will bring. Perhaps, rather that looking at Southampton alone, it's instructive to consider AGS as a whole, Southampton being the smallest airport of the group. Recovery from the pandemic is not great, but neither is it a disaster.

Join Date: Dec 2011

Location: South

Age: 44

Posts: 774

Likes: 0

Received 0 Likes

on

0 Posts

Based on the CAA numbers earlier in the thread, this isn�t looking great. The rolling annual pax figures should be showing some half decent upward trend if the easyJet BFS and GLA flights are truly creating a new market. They�re nearly static which says loud and clear that all easyJet has done so far is cannibalise passenger numbers from existing operators, exactly as I had feared.

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

What a mess. You have easyJet therefore not doing particularly well and a very pissed off bunch of existing airlines like Loganair and Emerald who will be raging at the airport management. Who is responsible for this mess?

Let me post it again:

�Interestingly the BHD route saw a 12% increase in December to 7,080 passengers despite EZY operating to BFS with 2,638. Proof that EZY doesn�t always take passengers away from other carriers?�

What do you have to say faced with the indisputable facts above?

Join Date: Jul 2002

Location: In the sticks

Posts: 9,863

Likes: 0

Received 0 Likes

on

0 Posts

In January BHD was down 4%, GLA up 6%.(both carriers combined)

By comparison where EZY don’t compete. EDI was down 21%, NCL also down 21%, Jersey down 9%, Guernsey up 1%, Alderney down 6%, Manchester down 100%

By comparison where EZY don’t compete. EDI was down 21%, NCL also down 21%, Jersey down 9%, Guernsey up 1%, Alderney down 6%, Manchester down 100%

Last edited by LTNman; 22nd Mar 2024 at 05:12.

Join Date: Mar 2004

Location: Dorset

Posts: 677

Likes: 0

Received 0 Likes

on

0 Posts

Several things to say. The first is that I had not clocked your earlier post, so can truthfully say the answer to your indignant �did you not see this� post is that I indeed had not. These things do happen.

The second point is that after seeing your post, I went back to the CAA statistics to make sure I wasn�t missing anything more. We now have six data points (three months Nov/Dec/Jan for two routes, GLA & BFS) to take a view on how this is going.

The one data point of the six you�ve called out is the only one which supports your view. The other five all support mine. So whilst you are correct in saying easyJet doesn�t always eat into traffic of other airlines, the weight of evidence is that for most of the time, it does.

Thirdly, have a look at the stats. easyJet�s January pax per flight on BFS (using the CAA OTP stats for the number of sectors flown) is 89. Even if all are its smallest aircraft then that�s a 57% load factor which is 25 points below its network average for the time of year. That�s an awful performance.

It�s harder to tell on Glasgow exactly what the situation between the two carriers is, but the January figures show Loganair operating 143 sectors versus last year�s 144 (so to all intents and purposes, the same). When you tot this up, seat capacity on GLA-SOU has increased by 40% in January but pax numbers have increased by only 15%. Nearly 3,000 more seats have gone into the market for a net growth of 700 more passengers carried.

If easyJet is carrying the same number of pax per flight on GLA as BFS (an assumption in the absence of any other data) then its load factor is similarly awful at about 57% and Loganair�s has dropped from 74% to 60%.

Fourthly, if you look at revenues, average selling fares have dropped certainly on the days when easyJet is flying (and those days are about to increase as we go into the summer schedule). If the average fare has dropped by 15% and volume goes up by 15%, total income from the route has stood still. But there are more aircraft flying with more direct operating costs to be covered than before.

To use an American phrase beloved of a different commentary site, this is a total dumpster fire. The economics of this for both the existing airlines and easyJet look awful, and for the airport, it has certainly singed if not burned bridges on all sides.

So accepting that there is one piece of data out of six which says things might be OK, the other five bits of data all paint a picture of a market in total turmoil and airline economics on all sides under serious stress. I stick by my views.

The vehemence of your reply does make me wonder if you work for AGS though!

The second point is that after seeing your post, I went back to the CAA statistics to make sure I wasn�t missing anything more. We now have six data points (three months Nov/Dec/Jan for two routes, GLA & BFS) to take a view on how this is going.

The one data point of the six you�ve called out is the only one which supports your view. The other five all support mine. So whilst you are correct in saying easyJet doesn�t always eat into traffic of other airlines, the weight of evidence is that for most of the time, it does.

Thirdly, have a look at the stats. easyJet�s January pax per flight on BFS (using the CAA OTP stats for the number of sectors flown) is 89. Even if all are its smallest aircraft then that�s a 57% load factor which is 25 points below its network average for the time of year. That�s an awful performance.

It�s harder to tell on Glasgow exactly what the situation between the two carriers is, but the January figures show Loganair operating 143 sectors versus last year�s 144 (so to all intents and purposes, the same). When you tot this up, seat capacity on GLA-SOU has increased by 40% in January but pax numbers have increased by only 15%. Nearly 3,000 more seats have gone into the market for a net growth of 700 more passengers carried.

If easyJet is carrying the same number of pax per flight on GLA as BFS (an assumption in the absence of any other data) then its load factor is similarly awful at about 57% and Loganair�s has dropped from 74% to 60%.

Fourthly, if you look at revenues, average selling fares have dropped certainly on the days when easyJet is flying (and those days are about to increase as we go into the summer schedule). If the average fare has dropped by 15% and volume goes up by 15%, total income from the route has stood still. But there are more aircraft flying with more direct operating costs to be covered than before.

To use an American phrase beloved of a different commentary site, this is a total dumpster fire. The economics of this for both the existing airlines and easyJet look awful, and for the airport, it has certainly singed if not burned bridges on all sides.

So accepting that there is one piece of data out of six which says things might be OK, the other five bits of data all paint a picture of a market in total turmoil and airline economics on all sides under serious stress. I stick by my views.

The vehemence of your reply does make me wonder if you work for AGS though!

Join Date: Mar 2004

Location: Dorset

Posts: 677

Likes: 0

Received 0 Likes

on

0 Posts

Indeed, results can be skewed by factors such as weather disruption and the like. But I think the point I�d make is that if you come back in 12 months time, the situation may well be beyond salvation far sooner than that timeline plays out.