QF shares hit $2.00, discuss

Join Date: Jun 2001

Location: Living next door to Alan

Posts: 1,521

Likes: 0

Received 0 Likes

on

0 Posts

Putting an androgyne draped in an Aussie flag won't help 'em, Tim

Qantas does not recognise goodwill, Gobbler. Well, not at EBA time at least. So, because it doesn't exist, he cannot depend on a non-existent quality in his staff to help him out

Will you call on the 'good will' of the staff to help bail you out?

"...the traumatic confrontation with three of its unions that cost it almost $200 million in the December half"

On the day of the AGM, 28th October 2011, Qantas claimed that the industrial action had cost $68 million. That looked like an exaggerated number, too. Since then, there has been a 48 hour long 'own goal' and then all has been compulsory rosiness in the industrial garden. Curious.

Join Date: Aug 2011

Location: goulburn

Posts: 393

Likes: 0

Received 0 Likes

on

0 Posts

And the next likely step is the ambulance chasing class action lawyers who must be salivating at the prospect of taking on this Board.

How long can this board sit back and watch the spiral dive being orchestrated or are they the architects? They can hardly claim they are just like everyone else now after being on a far superior position once that was not so long ago.

There surely must be an analogy to Kodak somewhere in all of this.

How long can this board sit back and watch the spiral dive being orchestrated or are they the architects? They can hardly claim they are just like everyone else now after being on a far superior position once that was not so long ago.

There surely must be an analogy to Kodak somewhere in all of this.

Join Date: Oct 2009

Location: Alabama, then Wyoming, then Idaho and now staying with Kharon on Styx houseboat

Age: 61

Posts: 1,437

Likes: 0

Received 0 Likes

on

0 Posts

Aagh yes the good old 'Board'. I always wondered how a bureaucratic bloated former Army General makes for a good board member?

And as for the hyped up highly fantasized appointment of Fyfe to replace the 'Irish airline destroyer' it's just not going to happen.

QF is now well and truly beyond saving, it now needs salvaging. And that will only be accomplished by the disposal of the executive team and their lap dog Board members. It will take an executive team of savvy, strategic knowledgeable aviation business minds to turn QF around, anybody know any potential candidates as none currently work for QF.

It seems that the term 'accountable manager' certainly doesn't apply to the current CEO. Perhaps 'untouchable manager' is more appropriate?

And as for the hyped up highly fantasized appointment of Fyfe to replace the 'Irish airline destroyer' it's just not going to happen.

QF is now well and truly beyond saving, it now needs salvaging. And that will only be accomplished by the disposal of the executive team and their lap dog Board members. It will take an executive team of savvy, strategic knowledgeable aviation business minds to turn QF around, anybody know any potential candidates as none currently work for QF.

It seems that the term 'accountable manager' certainly doesn't apply to the current CEO. Perhaps 'untouchable manager' is more appropriate?

Qantas will be "taken off the shareholders hands" by James Packer and the rest of the APA team, nothing surer.

Gillard has just been shafted by the licenced clubs and Packer over the pokies pre commitment thing, she will not want a repeat.

Once Qantas is in private hands, they will lobby like mad for industry protection, and they will get it.

Airlines are very, very good investments.........................................

.

.

.

......................................................if you pay chicken feed for them.

Gillard has just been shafted by the licenced clubs and Packer over the pokies pre commitment thing, she will not want a repeat.

Once Qantas is in private hands, they will lobby like mad for industry protection, and they will get it.

Airlines are very, very good investments.........................................

.

.

.

......................................................if you pay chicken feed for them.

Join Date: Apr 2009

Location: London-Thailand-Australia

Age: 15

Posts: 1,057

Received 0 Likes

on

0 Posts

It seems that the term 'accountable manager' certainly doesn't apply to the current CEO. Perhaps 'untouchable manager' is more appropriate?

IR battle sees Qantas pay price in market share

QANTAS mainline's share of the international market slumped to less than 18 per cent last October under the impact of industrial action that ultimately prompted it to ground its fleet at the end of that month.

Government international airline statistics released yesterday show the carrier's share of the market into and out of Australia fell almost two percentage points, to 17.6 per cent, as several major competitors gained ground.

The fall dragged down the overall share held by all Australian-designated airlines from 34 per cent to 32.9 per cent, with Pacific Blue at 5.1 per cent, V Australia at 1.8 per cent and Strategic Airlines at 0.6 per cent.

The Qantas Group -- which includes mainline and Jetstar international operations as well as Jetstar Asia -- accounted for 25.8 per cent of the market, down from 27.5 per cent the previous year. This compared with 9 per cent at Singapore Airlines, 8.9 per cent at Air New Zealand and 8.1 per cent at Emirates.

Overall, international scheduled passenger traffic for the month was up 4.1 per cent, to 2.471 million.

However, a 7.7 per cent rise in the number of available seats meant overall seat utilisation fell from 79.2 per cent in October 2010 to 76.7 per cent last October.

Low-cost carriers accounted for 19.2 per cent of the market, down from 19.4 per cent in the previous period. They plan to add flights later this year, with new services from Malaysia's AirAsia X and Singaporean-based Scoot.

The figures were revealed as Garuda Indonesia said it would expand its network routes and frequencies throughout Asia after strong passenger movements from Australia and the region.

This included a a 12 per cent increase in outbound passengers on Australia-Jakarta routes

- by: Steve Creedy, Aviation writer

- From: The Australian

- February 02, 2012 12:00AM

QANTAS mainline's share of the international market slumped to less than 18 per cent last October under the impact of industrial action that ultimately prompted it to ground its fleet at the end of that month.

Government international airline statistics released yesterday show the carrier's share of the market into and out of Australia fell almost two percentage points, to 17.6 per cent, as several major competitors gained ground.

The fall dragged down the overall share held by all Australian-designated airlines from 34 per cent to 32.9 per cent, with Pacific Blue at 5.1 per cent, V Australia at 1.8 per cent and Strategic Airlines at 0.6 per cent.

The Qantas Group -- which includes mainline and Jetstar international operations as well as Jetstar Asia -- accounted for 25.8 per cent of the market, down from 27.5 per cent the previous year. This compared with 9 per cent at Singapore Airlines, 8.9 per cent at Air New Zealand and 8.1 per cent at Emirates.

Overall, international scheduled passenger traffic for the month was up 4.1 per cent, to 2.471 million.

However, a 7.7 per cent rise in the number of available seats meant overall seat utilisation fell from 79.2 per cent in October 2010 to 76.7 per cent last October.

Low-cost carriers accounted for 19.2 per cent of the market, down from 19.4 per cent in the previous period. They plan to add flights later this year, with new services from Malaysia's AirAsia X and Singaporean-based Scoot.

The figures were revealed as Garuda Indonesia said it would expand its network routes and frequencies throughout Asia after strong passenger movements from Australia and the region.

This included a a 12 per cent increase in outbound passengers on Australia-Jakarta routes

- The Wall Street Journal

- January 31, 2012 9:10AM

AUSTRALIANS are packing their bags for overseas vacations like they've never done before. The trend, fuelled by the strong Australian dollar, is a boon for Qantas Airways and its low-cost Jetstar brand. Unfortunately for the flying kangaroo, other airlines are preparing to hop all over its turf.

Jetstar contributed 26 per cent of Qantas's earnings before interest and taxes in the year to June 30 -- $169 million out of a total of $644m. The unit has benefited from an about 50 per cent increase in Australians travelling overseas in the past five years.

But other low-cost carriers are also planning to shuttle Australians to holiday destinations in Southeast Asia too. From the middle of this year, Scoot -- owned by Singapore Airlines -- will fly 400 seats a day between Sydney and Asia.

A bigger threat might be Air Asia X, a unit of Malaysia's AirAsia, Southeast Asia's largest budget carrier by fleet size. Air Asia X recently pulled out of destinations in Europe, citing high taxes, and the company pledged to grow its business in Asia and Australia. It will start flying from Sydney to Kuala Lumpur in April, with promotional one-way tickets as low as around $60.

Qantas is not well-positioned to put up a fight.

Profit for the six months ended December 31 is expected to drop by more than half from the same period in 2010, with higher fuel costs and industrial action costing $650m.

Management's plan to stem losses on international flights by launching a premium regional airline in Asia has yet to get off the ground. Instead, it caused strikes that were stopped only after chief executive officer Alan Joyce grounded the entire fleet in October, a move that tested the patience and loyalty of passengers.

Competition also looms in the domestic business class market. Virgin Australia this month started offering business class seats on popular routes between Sydney, Melbourne and Brisbane with ticket prices as much as 30 per cent below market rates.

Qantas says competition is nothing new.

It's adding new aircraft to Jetstar and expanding its network too. But cut-rate promotions and increased capacity will bite into pricing. Australian travelers will benefit from the turf war.

But Qantas surely won't.

Jetstar contributed 26 per cent of Qantas's earnings before interest and taxes in the year to June 30 -- $169 million out of a total of $644m. The unit has benefited from an about 50 per cent increase in Australians travelling overseas in the past five years.

But other low-cost carriers are also planning to shuttle Australians to holiday destinations in Southeast Asia too. From the middle of this year, Scoot -- owned by Singapore Airlines -- will fly 400 seats a day between Sydney and Asia.

A bigger threat might be Air Asia X, a unit of Malaysia's AirAsia, Southeast Asia's largest budget carrier by fleet size. Air Asia X recently pulled out of destinations in Europe, citing high taxes, and the company pledged to grow its business in Asia and Australia. It will start flying from Sydney to Kuala Lumpur in April, with promotional one-way tickets as low as around $60.

Qantas is not well-positioned to put up a fight.

Profit for the six months ended December 31 is expected to drop by more than half from the same period in 2010, with higher fuel costs and industrial action costing $650m.

Management's plan to stem losses on international flights by launching a premium regional airline in Asia has yet to get off the ground. Instead, it caused strikes that were stopped only after chief executive officer Alan Joyce grounded the entire fleet in October, a move that tested the patience and loyalty of passengers.

Competition also looms in the domestic business class market. Virgin Australia this month started offering business class seats on popular routes between Sydney, Melbourne and Brisbane with ticket prices as much as 30 per cent below market rates.

Qantas says competition is nothing new.

It's adding new aircraft to Jetstar and expanding its network too. But cut-rate promotions and increased capacity will bite into pricing. Australian travelers will benefit from the turf war.

But Qantas surely won't.

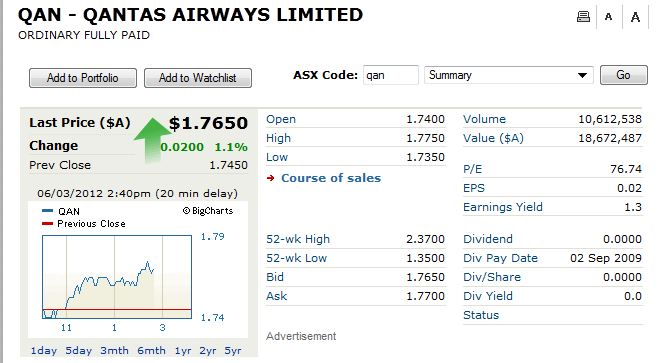

Having said that, I note the share price jumped today

Last Price ($A) $1.6150 Change 0.0550 3.5% Prev Close 1.5600 Is someone buying up?

meanwhile

Rob Fyfe | Air New Zealand Boss Won't Work For Rivals... | Stuff.co.nz

Fyfe said he had no idea what he would do next and dismissed conjecture that he had been offered a position at Sir Richard Branson's Virgin Atlantic airline, he did rule out working for any of Air New Zealand's close competitors.

Join Date: Dec 2001

Location: Always changing

Posts: 202

Likes: 0

Received 0 Likes

on

0 Posts

There will be many bounces on the way to the bottom. Nothing moves in a straight line so they say. I'm sure Qantas will look like a bargain many times on the way to sub $1. Just like it was a bargain at $2 and at $1.75 for many experts.

Qantas cost cutting 2012.

FRA gone, JFK gone.

Bookies offering extremely short odds on the AKL-LAX route survivability.

And the saviour Jetstar not delivering as expected, but seen as the only way forward.

What a strategy.

FRA gone, JFK gone.

Bookies offering extremely short odds on the AKL-LAX route survivability.

And the saviour Jetstar not delivering as expected, but seen as the only way forward.

What a strategy.

Join Date: Feb 2007

Location: Melbourne

Age: 57

Posts: 628

Likes: 0

Received 0 Likes

on

0 Posts

What a strategy indeed!

Then add this bit in...

Flying Qantas just got more expensive

And they wonder why customers are disgruntled. When I have a choice it's Virgin/Singapore as often as possible these days.

Then add this bit in...

Flying Qantas just got more expensive

And they wonder why customers are disgruntled. When I have a choice it's Virgin/Singapore as often as possible these days.

Join Date: Oct 2011

Location: Melbourne

Age: 38

Posts: 13

Likes: 0

Received 0 Likes

on

0 Posts

Qantas cost cutting 2012.

FRA gone, JFK gone.

Bookies offering extremely short odds on the AKL-LAX route survivability.

FRA gone, JFK gone.

Bookies offering extremely short odds on the AKL-LAX route survivability.

JFK was recently bumped back up to daily and Joyce stated in the media last September that it had become profitable since QF switched from the Jumbo to the A332. I'd hate for them to drop this flight - it's easily the best way to/from New York. What data is out there to indicate how well a route is performing (other than the tell-tale cancellations on 3K's SIN-AKL)?

Join Date: Dec 2007

Location: Downunder

Age: 74

Posts: 257

Likes: 0

Received 0 Likes

on

0 Posts

Over the coming days and weeks a number of airlines are likely to follow Qantas's lead and release media statements explaining why they must increase ticket prices to recover higher fuel and carbon costs, to the dismay of the embattled consumer.

If this columnist were composing the media releases, however, I wouldn't be making any mention of raising ticket prices. That's because hiking airfares, in isolation, won't recover higher fuel and carbon costs.

Instead, I would have said that the airline expects to reduce the number of seats that it flies compared with planned levels by between 1 per cent and 2 per cent.

Advertisement: Story continues below

There are a number of reasons why reducing the number of seats is the right strategy in response to higher fuel costs and raising ticket prices in isolation won't work.

Price sensitive demand

Let's start with why more costly airfares won't work.

For higher ticket prices to work, the airline must be confident that its revenue will go up. This is no certainty because when prices go up demand goes down.

If domestic airfares increase by 2.5 per cent on average then revenue will only go up if demand falls by less than 2.5 per cent (economists call this price-inelastic demand).

If demand falls by more than 2.5 per cent (ie demand is relatively elastic) then airlines would be in the nasty position of facing higher costs and lower revenue - not a good outcome for the bottom line.

In a weak, uncertain economic environment like we have at the moment, the risk that demand will fall by more than 2.5 per cent is elevated because people become more price sensitive when they are less secure about their jobs.

The situation now is diametrically opposite to that before the global financial crisis struck. In that environment raising ticket prices was like printing money because demand was so insensitive to price. Not so anymore.

Seat factor target

It is also conceivable that the average airfare may not increase at all even though advertised ticket prices are lifted.

This will happen if the airline rigidly targets a particular seat factor (the percentage of seats filled with passengers).

For example, if the airline operates 100 seats and targets a seat factor of 80 per cent then it wishes to convince 80 people to fly on the plane. It can do this at an average airfare of $100. If it tries to add a surcharge of $2.50 then 5 people will stop flying and the seat factor falls to 75 per cent.

To restore the targeted seat factor of 80 per cent the airline must convince 5 more people to fly, which will require the base airfare to fall back by $2.50 so there is no net gain in the total airfare and no ability to recover higher fuel costs.

Implied irrationality

A strategy of raising ticket prices because of higher fuel prices also implies that the airline was behaving irrationally before fuel prices went up.

The thinking here is that if the conditions that generate extra revenue from higher average airfares were around after the increase in fuel prices then they would have been around before the increase in fuel prices.

So why didn't the airline put ticket prices up before fuel prices went up if that was going to make it more money?

Let capacity fall

Reducing capacity both reduces fuel costs and forces up average airfares. Fuel costs go down because fuel consumption falls and fuel consumption falls because it is positively linked to the number of seats that are flown.

Average airfares (not advertised ticket prices) go up because the same demand is squeezed into fewer seats, which means some people will be forced into higher price buckets. This raises average airfares.

Other variable costs also fall because most costs vary with the number of seats, and this is now lower.

A strategy of capacity reduction reduces costs by more than it cuts revenue, which results in more profit.

Airlines are extremely reluctant to reduce seats, because they don't want to run the risk of conceding market share to competitors. Sometimes they need to learn, however, to look after their own backyard and let others worry about theirs.

If this columnist were composing the media releases, however, I wouldn't be making any mention of raising ticket prices. That's because hiking airfares, in isolation, won't recover higher fuel and carbon costs.

Instead, I would have said that the airline expects to reduce the number of seats that it flies compared with planned levels by between 1 per cent and 2 per cent.

Advertisement: Story continues below

There are a number of reasons why reducing the number of seats is the right strategy in response to higher fuel costs and raising ticket prices in isolation won't work.

Price sensitive demand

Let's start with why more costly airfares won't work.

For higher ticket prices to work, the airline must be confident that its revenue will go up. This is no certainty because when prices go up demand goes down.

If domestic airfares increase by 2.5 per cent on average then revenue will only go up if demand falls by less than 2.5 per cent (economists call this price-inelastic demand).

If demand falls by more than 2.5 per cent (ie demand is relatively elastic) then airlines would be in the nasty position of facing higher costs and lower revenue - not a good outcome for the bottom line.

In a weak, uncertain economic environment like we have at the moment, the risk that demand will fall by more than 2.5 per cent is elevated because people become more price sensitive when they are less secure about their jobs.

The situation now is diametrically opposite to that before the global financial crisis struck. In that environment raising ticket prices was like printing money because demand was so insensitive to price. Not so anymore.

Seat factor target

It is also conceivable that the average airfare may not increase at all even though advertised ticket prices are lifted.

This will happen if the airline rigidly targets a particular seat factor (the percentage of seats filled with passengers).

For example, if the airline operates 100 seats and targets a seat factor of 80 per cent then it wishes to convince 80 people to fly on the plane. It can do this at an average airfare of $100. If it tries to add a surcharge of $2.50 then 5 people will stop flying and the seat factor falls to 75 per cent.

To restore the targeted seat factor of 80 per cent the airline must convince 5 more people to fly, which will require the base airfare to fall back by $2.50 so there is no net gain in the total airfare and no ability to recover higher fuel costs.

Implied irrationality

A strategy of raising ticket prices because of higher fuel prices also implies that the airline was behaving irrationally before fuel prices went up.

The thinking here is that if the conditions that generate extra revenue from higher average airfares were around after the increase in fuel prices then they would have been around before the increase in fuel prices.

So why didn't the airline put ticket prices up before fuel prices went up if that was going to make it more money?

Let capacity fall

Reducing capacity both reduces fuel costs and forces up average airfares. Fuel costs go down because fuel consumption falls and fuel consumption falls because it is positively linked to the number of seats that are flown.

Average airfares (not advertised ticket prices) go up because the same demand is squeezed into fewer seats, which means some people will be forced into higher price buckets. This raises average airfares.

Other variable costs also fall because most costs vary with the number of seats, and this is now lower.

A strategy of capacity reduction reduces costs by more than it cuts revenue, which results in more profit.

Airlines are extremely reluctant to reduce seats, because they don't want to run the risk of conceding market share to competitors. Sometimes they need to learn, however, to look after their own backyard and let others worry about theirs.

So what idiot who obviously knows nothing about airlines came up with these ridiculous ideas ?

Tony Webber was Qantas Group chief economist between 2004 and 2011.

He is now managing director of Webber Quantitative Consulting and Associate Professor at the University of Sydney Business School.

http://www.businessday.com.au/business/careful-with-those-airfare-hikes-20120203-1qw72.html

Maybe he does know a thing or two about airline finances !!

ST

He used to work for Qantas, that much is obvious:

But reduce capacity to zero and the profit does not become infinite, alas.

All this might work in a monopoly or cosy duopoly. Unfortunately, it makes no sense in a voracious multi-player market as exists longhaul out of Australia. You just get eaten up and spat out.

Let capacity fall

Reducing capacity both reduces fuel costs and forces up average airfares. Fuel costs go down because fuel consumption falls and fuel consumption falls because it is positively linked to the number of seats that are flown.

Average airfares (not advertised ticket prices) go up because the same demand is squeezed into fewer seats, which means some people will be forced into higher price buckets. This raises average airfares.

Other variable costs also fall because most costs vary with the number of seats, and this is now lower.

A strategy of capacity reduction reduces costs by more than it cuts revenue, which results in more profit.

Reducing capacity both reduces fuel costs and forces up average airfares. Fuel costs go down because fuel consumption falls and fuel consumption falls because it is positively linked to the number of seats that are flown.

Average airfares (not advertised ticket prices) go up because the same demand is squeezed into fewer seats, which means some people will be forced into higher price buckets. This raises average airfares.

Other variable costs also fall because most costs vary with the number of seats, and this is now lower.

A strategy of capacity reduction reduces costs by more than it cuts revenue, which results in more profit.

All this might work in a monopoly or cosy duopoly. Unfortunately, it makes no sense in a voracious multi-player market as exists longhaul out of Australia. You just get eaten up and spat out.

Or it would work if you had great customer loyalty and the best product. The same reasons why Grange can be sold for any amount of money. It's very good and there are only so many of it.

If it wasn't very good or if there was lots of it, it would lose the value.

If it wasn't very good or if there was lots of it, it would lose the value.

So what idiot who obviously knows nothing about airlines came up with these ridiculous ideas ?

Tony Webber was Qantas Group chief economist between 2004 and 2011.

He is now managing director of Webber Quantitative Consulting and Associate Professor at the University of Sydney Business School.

http://www.businessday.com.au/business/careful-with-those-airfare-hikes-20120203-1qw72.html

Maybe he does know a thing or two about airline finances !!

Tony Webber was Qantas Group chief economist between 2004 and 2011.

He is now managing director of Webber Quantitative Consulting and Associate Professor at the University of Sydney Business School.

http://www.businessday.com.au/business/careful-with-those-airfare-hikes-20120203-1qw72.html

Maybe he does know a thing or two about airline finances !!

One wonders why he left Qantas with gems like that one!

'Those who can, do. Those who can't, teach' comes to mind.

Join Date: Jun 2007

Location: Airborne

Posts: 203

Likes: 0

Received 0 Likes

on

0 Posts

My goodness, there's so many things wrong with that article I don't know where to start.

At least there's another explanation of what has been wrong with QF this past decade with muppets like these running the show.

About the only thing you save by reducing capacity is fuel. Most other costs are fixed (leases, staff, infrastructure etc) so all you achieve is to increase the cost of your remaining ASKs.

The implied irrationality argument doesn't wash either because your competitors are faced with the same rising fuel prices as yourself.

I'm surprised he didn't mention that B777's can't make money.

At least there's another explanation of what has been wrong with QF this past decade with muppets like these running the show.

About the only thing you save by reducing capacity is fuel. Most other costs are fixed (leases, staff, infrastructure etc) so all you achieve is to increase the cost of your remaining ASKs.

The implied irrationality argument doesn't wash either because your competitors are faced with the same rising fuel prices as yourself.

I'm surprised he didn't mention that B777's can't make money.

Join Date: May 2008

Location: oz

Posts: 106

Likes: 0

Received 0 Likes

on

0 Posts

From the Rumours and News section.

American Airlines: We'll have 'many fewer' jobs - Feb. 1, 2012.

A lot of similarities. Aren't QF in bed with this mob?

American Airlines: We'll have 'many fewer' jobs - Feb. 1, 2012.

A lot of similarities. Aren't QF in bed with this mob?

Join Date: Apr 2009

Location: London-Thailand-Australia

Age: 15

Posts: 1,057

Received 0 Likes

on

0 Posts

Qantas Shares - something's up

Interesting figures today.... Qantas is up whilst the market is down.... announcement coming? Seems like something is brewing..

.