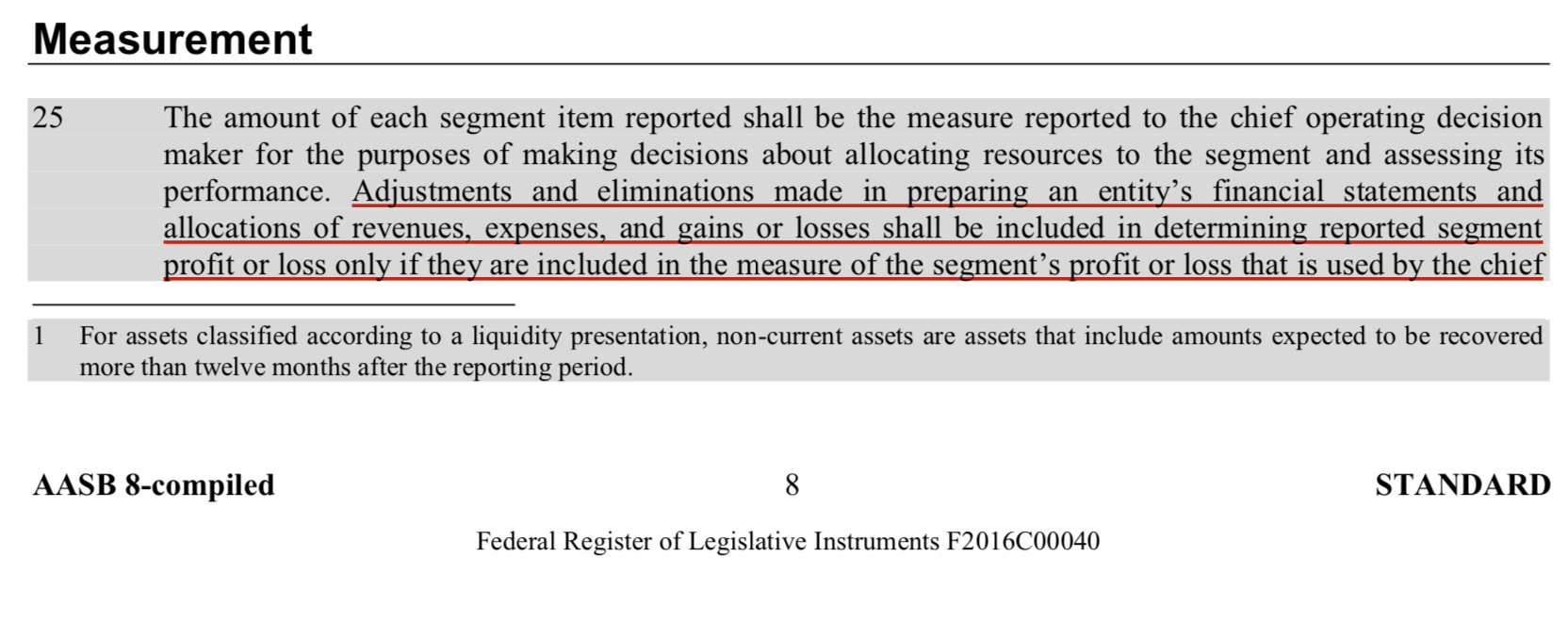

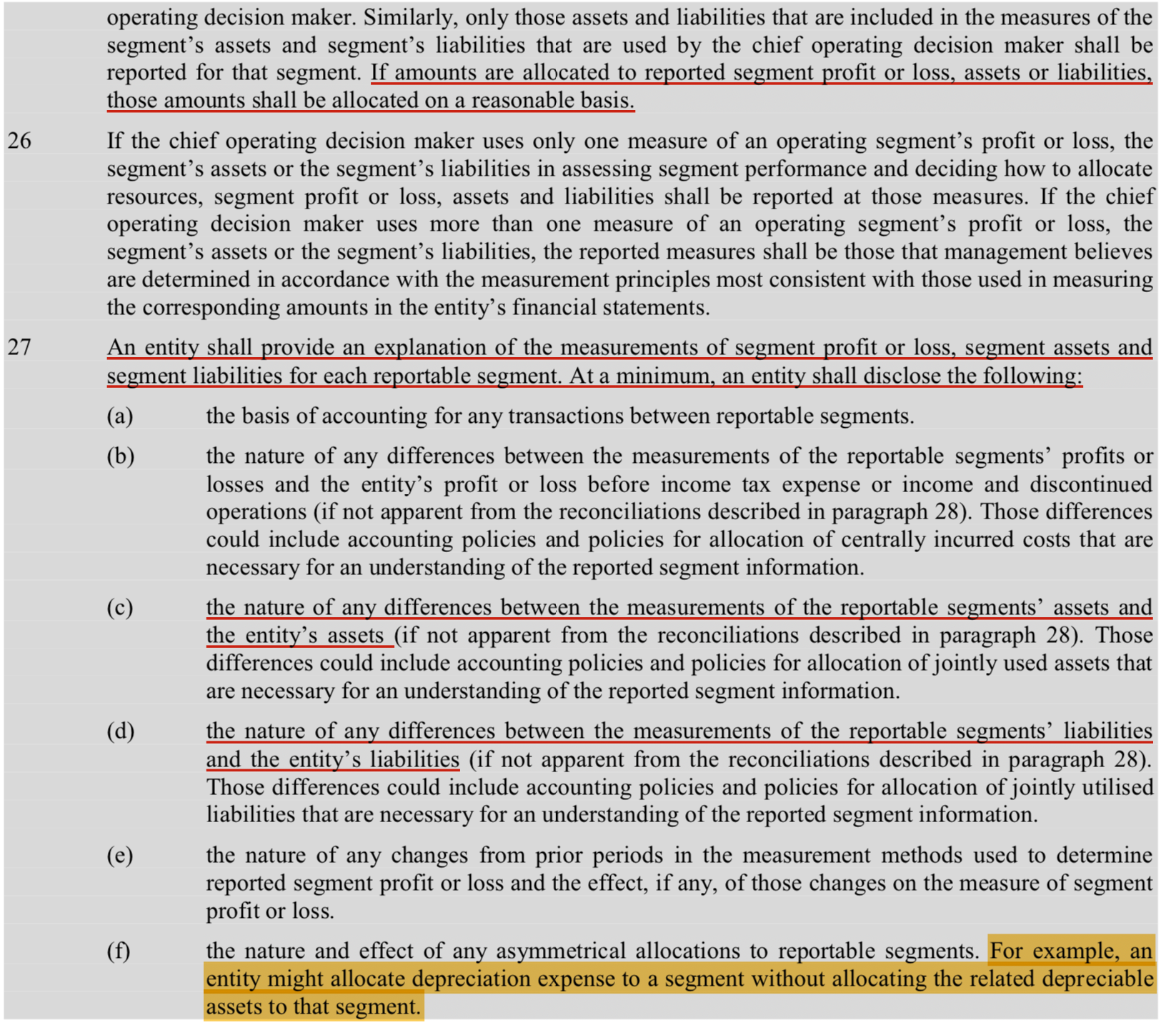

Read the

Australian Accounting Standard on segment accounting. AASB8 and decide for yourself.

As an outsider, corporate accounting looks a bit like the responsibility of a Pilot In Command. Lots of general rules and principles, but ultimately a lot of flexibility to run the Corporation in a non-prescriptive (from a legal perspective) manner as the "Chief Operating Decision Maker" deems fit.

My interpretation of the rules is this: You have lots of flexibility to arrange your segments how you deem fit, and

note how you did it in your segment accounts. However,

those segment account notes are not required to be disclosed in the aggregated financial report. This subtle difference in reporting requirements is the crack that Qantas wedged open to drive the proverbial truck through for industrial relations purposes.

There is no contradiction between shifting revenues and costs between entities "

on a reasonable basis", turning profitable internal entities into loss making ones and vice versa, and making public statements to that effect. Without the accounting report & notes and the basis of those shifts it is impossible to actually determine what really happens in each entity. Qantas could choose to report those internal segment accounts, however they don't. Therefore, public statements on the profitability of

any internal entity is on a "trust us" on what is a "reasonable" basis.

But you don't need to take my word for it, read the standard yourself and draw your own conclusions.