Pension Horror - Annual Allowance

But isn’t that the point VinRouge - there is no risk with AFPS (apart from some sort of armageddon) whereas even with the most stable private plans there is always risk of collapse. Ask Mrs LJ, her private pension pot, in a low risk private pension scheme, was roughly Ł0.5M prior to 2007, it is now worth less than Ł0.2M. Whereas, my AFPS was totally unaffected by the various market crashes (save for the auto enrolment onto AFPS15, although I am better off on that as I get the ability to earn pension past 55 now that I didn’t on AFPS75).

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

But isn’t that the point VinRouge - there is no risk with AFPS (apart from some sort of armageddon) whereas even with the most stable private plans there is always risk of collapse. Ask Mrs LJ, her private pension pot, in a low risk private pension scheme, was roughly Ł0.5M prior to 2007, it is now worth less than Ł0.2M. Whereas, my AFPS was totally unaffected by the various market crashes (save for the auto enrolment onto AFPS15, although I am better off on that as I get the ability to earn pension past 55 now that I didn’t on AFPS75).

People are now being taxed on contributions to the scheme despite not having an actual pot. It’s the flip side to the same coin.

The key key point is diversification across assets and not putting eggs in one basket, with differing levels of risk in the pot.

Vin Rouge / L J,

Just so my thinking is correct......

A workplace pension/SIPP etc sees money invested-and at the end, you get what you get depending on how your “pot” performs.

AFPS works backwards-your return is guaranteed, and the GAD works out what it thinks you should pay in (to a civilian equivalent) to receive the guaranteed return.

If so-then the GAD must be assuming a pretty poor performing “fund” if it thinks contributions need to be that high. What growth assumptions are behind the SCAPE contributions? If its none, or just a few percent, then no wonder the contributions are so high. I would expect a healthy couple of percent above inflation from any invested pension pot. Is SCAPE simply writing an IOU for a modest amount of interest up front and putting that in the IOU pot for later?

The benefits of compound interest can be huge over time on any workplace pension/SIPP. Just two % above inflation will see any pot of money double in 35 years, or 3% about will double in just over 20.

Diversifying your portfolio in a SIPP spreads risk and allows you to “take the rough with the smooth” especially if you have time on your side. I totally get that the AFPS is risk free (save armageddon) though.

LJ-hope Mrs LJ’s pot enjoys better luck soon.

Regarding my Lifetime allowance in your response to my post the other day-I did recently receive my annual pension statement. It had my “ value of your benefit against LTA limit” down as “0” which I’m pretty sure is incorrect.

Just so my thinking is correct......

A workplace pension/SIPP etc sees money invested-and at the end, you get what you get depending on how your “pot” performs.

AFPS works backwards-your return is guaranteed, and the GAD works out what it thinks you should pay in (to a civilian equivalent) to receive the guaranteed return.

If so-then the GAD must be assuming a pretty poor performing “fund” if it thinks contributions need to be that high. What growth assumptions are behind the SCAPE contributions? If its none, or just a few percent, then no wonder the contributions are so high. I would expect a healthy couple of percent above inflation from any invested pension pot. Is SCAPE simply writing an IOU for a modest amount of interest up front and putting that in the IOU pot for later?

The benefits of compound interest can be huge over time on any workplace pension/SIPP. Just two % above inflation will see any pot of money double in 35 years, or 3% about will double in just over 20.

Diversifying your portfolio in a SIPP spreads risk and allows you to “take the rough with the smooth” especially if you have time on your side. I totally get that the AFPS is risk free (save armageddon) though.

LJ-hope Mrs LJ’s pot enjoys better luck soon.

Regarding my Lifetime allowance in your response to my post the other day-I did recently receive my annual pension statement. It had my “ value of your benefit against LTA limit” down as “0” which I’m pretty sure is incorrect.

AFPS 15 cost me and many in my generation over 1/3 of the original promise. And whilst we were unable to touch the pension and had to serve the remainder of the time on a scheme with a far lower accrual, it’s snake oil sales tactics to suggest we didn’t lose anything. That change cost my pension in the region of 100k, not accounting for CPI increases.

Professor Plum

This is what the recent valuation report stated on CPI in the report I linked to a few posts up from April 19:

” The SCAPE discount rate has been updated to reflect these changes and was reduced from 3.0% pa above CPI to 2.8% pa above CPI from April 2016 to April 2019 and was subsequently reduced to 2.4% pa above CPI. ”

LJ,

Thanks. I should’ve read the link instead of being lazy!

Thanks. I should’ve read the link instead of being lazy!

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

In the House of Lords on the 15 October our Vice President, Marshal of the Royal Air Force Lord Craig of Radley GCB OBE spoke about the effect of Annual Allowance on Forces personnel.

The post Annual Allowance in the House of Lords appeared first on Forces Pension Society.

The post Annual Allowance in the House of Lords appeared first on Forces Pension Society.

Thread Starter

Join Date: Oct 2019

Location: UK

Posts: 5

Likes: 0

Received 0 Likes

on

0 Posts

Doctors get their tax bills paid

I can’t post the URL because I’m a Newb, but the BBC online are running a story that the NHS is to pay the in-year pension tax bills for doctors in order to encourage them back to work.

i wonder if this will be replicated across the public sector? I wonder if our Senior Leadership has the courage to press the Treasury in the same way.

if not, I’ll be writing a Ł10000 cheque next month. No Christmas for me.

i wonder if this will be replicated across the public sector? I wonder if our Senior Leadership has the courage to press the Treasury in the same way.

if not, I’ll be writing a Ł10000 cheque next month. No Christmas for me.

Personally, I would sooner have Ł10,000 available now to enjoy Christmas with a young (ish) family than have a few hundred extra pounds to spend in each year of my dotage. But each to their own. I also take the view that cash payments would be harder to claw back should it ever be decided at some point in future that this whole episode was the result of an unfortunate oversight by those who introduced the changes, whereas notional pension pots could be restored at the click of a keyboard without the inconvenience of finding ready cash...

Last edited by Easy Street; 18th Nov 2019 at 21:42.

Join Date: Aug 2007

Location: on track, on speed, on time

Posts: 74

Likes: 0

Received 0 Likes

on

0 Posts

Useful 'scheme pays' summary here - https://forcespensionsociety.org/new...a-scheme-pays/

EDP is not considered during AA PIA calculations and is not relevant in this context. The principle of CPI growth on any 15 pension AA debt applies equally whether the example is AFPS 15/75 or AFPS 15/05.

Join Date: Oct 2005

Location: UK

Posts: 57

Likes: 0

Received 0 Likes

on

0 Posts

Uniformed Medical Officers warned of this affecting them years ago.

They were ignored and essentially told to suck it up, 'you don't you know how lucky you are'.

Uniformed Medical Officers warned of this affecting you years ago.

They were ignored.

Uniformed Medical Officers are leaving because of this.

They are being ignored.

There is no plan to implement the very specific NHS suggestion to Defence that we have been told about. I would suspect the NHS solution to be challenged in the courts by those in the same scheme with bills but that don't happen to be Doctors.

This has been a cluster from the start but sadly NO ONE LISTENED TO THE 'OVERPAID DOCTORS BLEATING'.

Sorry, forgot to say that that phrase was used too.

End of rant.

They were ignored and essentially told to suck it up, 'you don't you know how lucky you are'.

Uniformed Medical Officers warned of this affecting you years ago.

They were ignored.

Uniformed Medical Officers are leaving because of this.

They are being ignored.

There is no plan to implement the very specific NHS suggestion to Defence that we have been told about. I would suspect the NHS solution to be challenged in the courts by those in the same scheme with bills but that don't happen to be Doctors.

This has been a cluster from the start but sadly NO ONE LISTENED TO THE 'OVERPAID DOCTORS BLEATING'.

Sorry, forgot to say that that phrase was used too.

End of rant.

[QUOTE=VinRouge;10593249]

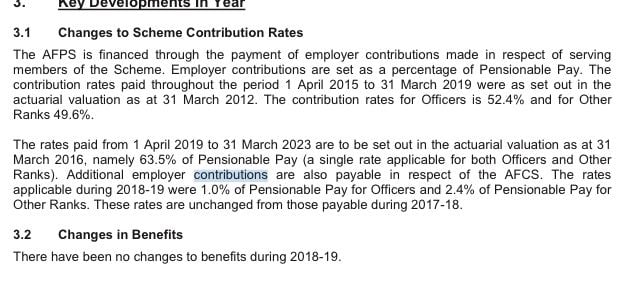

Re the above - about this time of year I chuck some coppers into my SIPP to recoup some of that 41% (Scottish resident) tax. To guess how much I can bung in, I need to know where I am in regard to the 40k Annual Allowance for FY19/20. I'm guessing I can roughly multiply my pensionable pay x 63.5% to get that figure. The question is, what constitutes 'pensionable pay' in this instance? Is it net income or gross inc NI or gross minus NI? No info on the interweb that I can find. Emailed JPAC / Veterans UK for a detailed quote but nothing heard back yet....

Re the above - about this time of year I chuck some coppers into my SIPP to recoup some of that 41% (Scottish resident) tax. To guess how much I can bung in, I need to know where I am in regard to the 40k Annual Allowance for FY19/20. I'm guessing I can roughly multiply my pensionable pay x 63.5% to get that figure. The question is, what constitutes 'pensionable pay' in this instance? Is it net income or gross inc NI or gross minus NI? No info on the interweb that I can find. Emailed JPAC / Veterans UK for a detailed quote but nothing heard back yet....

A couple of pals were briefed by Simone at Wycombe recently. This only affects 75 and 15, because before age 55 you’re looking at an EDP not a pension. Lots of facts and figs, but if you are going to get hit by this it is normally after a promotion. It then goes away. Don’t ask me why, but Wg Cdrs on flying pay, not PAS aren’t getting these letters.

A couple of pals were briefed by Simone at Wycombe recently. This only affects 75 and 15, because before age 55 you’re looking at an EDP not a pension. Lots of facts and figs, but if you are going to get hit by this it is normally after a promotion. It then goes away. Don’t ask me why, but Wg Cdrs on flying pay, not PAS aren’t getting these letters.

)

)

fprince - will let you know if I hear from VeteransUK Pensions division - email sent and acknowledged last week (asked for more info so that is promising). I've been adding to a SIPP for about 10 years but I am now very cautious about hitting the 40k max (including the 'virtual' AFPS contribution). Frustrating when we are trying to 'plan for the future' as per the govt's advice...

Join Date: Nov 2013

Location: stoke

Age: 61

Posts: 25

Likes: 0

Received 0 Likes

on

0 Posts

SP, many thanks for that, there are quite a few in one of the Whatsapp groups that are concentrating on this. I've recently asked my B&TA, who has a pretty good handle on all things finance, so if he says he doesn't fully understand it, then it's time for the paid experts. I did read yesterday, on one site, that it's common to receive the letter after a promotion, or at a pension point? I don't know where PAS fits into this, as it's circa Ł1100 each year. What this does do is focus my mind acutely to my PP, as whilst it's been said above that you will always be better off in our scheme, it takes away the 40% tax present that is so rare to find these days! Perhaps VR or ADC is the way ahead?! OR I could just retire as I've spent 33 years planning for!!

Just out of interest did the SoS for Defence say during the election it was one of things he wanted to sort, after he sorts the pipeline (RAF), ship availability and army recruitment?!!

Just out of interest did the SoS for Defence say during the election it was one of things he wanted to sort, after he sorts the pipeline (RAF), ship availability and army recruitment?!!

FP - PM'd you. For others interested, the figure I've been given (2018/19) works out at about 48% of my net pay. I'll be using the new '63%' rate (see articles above) of my net wage to guess this years 'contribution' and then top-up SIPP but keeping below 40k total contributions. Not having live data for current year isn't ideal when you can't retrospectively add to your SIPP to maximise your pension (as the govt says it encourages us to do....).

When the civvy pilots went along and protested to various government officials about the effect of this made up tax, we were informed that it was no accident, and that we, along with middle class professionals were most definitely the target. I’m pleased to say that the chickens are now coming home to roost.