Pension Horror - Annual Allowance

Ballistic Profile

Have a read of this chum, it might help explain some more for you: https://forcespensionsociety.org/new...-right-can-it/

The really good advice is this bit:

Have a read of this chum, it might help explain some more for you: https://forcespensionsociety.org/new...-right-can-it/

The really good advice is this bit:

Q. Many people say it is not worth me being promoted because of this!

A. You will always be better off as a result of promotion. We have had people talk about leaving the services to avoid the charge, opting out of the scheme or joining a different scheme. None of these are particularly good ideas. Someone who is promoted, and breaches, and pays a tax charge, will be better off financially than someone who does none of those things. What I say to people is it�s like joining the services and saying �I will stay as a corporal throughout my entire career because by doing so I will never pay tax at 40% � that�ll show �em!� Besides, if you leave to avoid this you will almost certainly have to take up some other career with a pension scheme which will be also subjected to annual allowance � it does not just apply exclusively to the Armed Forces!

A. You will always be better off as a result of promotion. We have had people talk about leaving the services to avoid the charge, opting out of the scheme or joining a different scheme. None of these are particularly good ideas. Someone who is promoted, and breaches, and pays a tax charge, will be better off financially than someone who does none of those things. What I say to people is it�s like joining the services and saying �I will stay as a corporal throughout my entire career because by doing so I will never pay tax at 40% � that�ll show �em!� Besides, if you leave to avoid this you will almost certainly have to take up some other career with a pension scheme which will be also subjected to annual allowance � it does not just apply exclusively to the Armed Forces!

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

VinRouge

So, I feel you may have made a very unsound decision if you left because you thought that pensions would be better in civilian life - the only way they would be better would be if you were paid about 60% more than your pensionable salary was in the Service.

So, I feel you may have made a very unsound decision if you left because you thought that pensions would be better in civilian life - the only way they would be better would be if you were paid about 60% more than your pensionable salary was in the Service.

So was the lack of a pay rise for a decade, as well as Royal protections removed from AFPS when the 15 change happened pretty much was a final nail in the coffin.

Since then, the discount rate has been changed, with impacts to the affordability of the scheme. And whilst you are right, they can�t take away accrued benefits, being part of a scheme that doesn�t permit you to realise those benefits until you have served a defined period on a significantly deteriorated accrual rate, through either TOS or pension point is downright unfair in the extreme. A fair way of dealing with the situation would have been to allow personnel to exit prior to IPP, but not pay out until the same time frame to IPP thereby allowing accrual externally whilst preserving pension rights for what was earned. Was that even considered? Nope. But I bet MoD/HMG wouldn�t now be in the dwang they are reference grandfather rights if they had. Would also be very interested to see what % of salary 90K is for an OF5 though.

Thread Starter

Join Date: Oct 2019

Location: UK

Posts: 5

Likes: 0

Received 0 Likes

on

0 Posts

VR - I can tell you, it�s more than 100%.

However, this �90k figure is my Pension Input Amount - ie what an actuary has estimated my notional input to a pension pot would be to generate the change in my predicted pension (over the last year).

i don�t yet know what the tax is that I�ll have to pay due to my �error� of paying into my notional pot more than the �40k allowance.

Anyone know what I might be about to be shaken down for?

However, this �90k figure is my Pension Input Amount - ie what an actuary has estimated my notional input to a pension pot would be to generate the change in my predicted pension (over the last year).

i don�t yet know what the tax is that I�ll have to pay due to my �error� of paying into my notional pot more than the �40k allowance.

Anyone know what I might be about to be shaken down for?

VR - I can tell you, it�s more than 100%.

However, this �90k figure is my Pension Input Amount - ie what an actuary has estimated my notional input to a pension pot would be to generate the change in my predicted pension (over the last year).

i don�t yet know what the tax is that I�ll have to pay due to my �error� of paying into my notional pot more than the �40k allowance.

Anyone know what I might be about to be shaken down for?

However, this �90k figure is my Pension Input Amount - ie what an actuary has estimated my notional input to a pension pot would be to generate the change in my predicted pension (over the last year).

i don�t yet know what the tax is that I�ll have to pay due to my �error� of paying into my notional pot more than the �40k allowance.

Anyone know what I might be about to be shaken down for?

I am genuinely surprised that this is the first time it�s happened to you.

I�ve just had a letter too. Ran it through the calculator and it looks like I�m being stung for in excess of 10k tax bill. I suspect many heard the expletives in the next county.

I owe this for doing nothing other than going to work and doing my job. I have no control over pay, hours worked or pension inputs. As an accidental OF4, I�m hardly up in the fat cat stakes the government intended to stop manipulating the pensions system. Cross doesn�t start to describe it.

I was aware of the issue, especially that OF4 is a vulnerable rank, but got onto FPS pretty pronto as this isn�t something you can plan your way out of. But when the literature implies a broadly linear increase to your pension - every pamphlet / briefing I�ve seen has said it goes up in line with salary and time served - I was stunned to see that the PIA is anything but linear. One year the govt put 5k into my pension and then last year in excess of 100k which has caused the problems. Other issues surround how to pay. If you pay up front and the govt changes the rules in 18 months you�ve just spanked a lot of money. But if you go down the scheme pays route and they treat it as a loan - I believe that is how it works for the NHS Scheme Pays rules - you end up paying interest on the loan, a loan which you�ve never actually had the benefit from.

Its a mess, and it will get worse if we all go back to 75 Scheme in a few years and we get another lump sum thrown at pensions as reparation. But hey, numbers are boyuant, morale�s good and the PVR rate tiny. What�s to worry about?!

I owe this for doing nothing other than going to work and doing my job. I have no control over pay, hours worked or pension inputs. As an accidental OF4, I�m hardly up in the fat cat stakes the government intended to stop manipulating the pensions system. Cross doesn�t start to describe it.

I was aware of the issue, especially that OF4 is a vulnerable rank, but got onto FPS pretty pronto as this isn�t something you can plan your way out of. But when the literature implies a broadly linear increase to your pension - every pamphlet / briefing I�ve seen has said it goes up in line with salary and time served - I was stunned to see that the PIA is anything but linear. One year the govt put 5k into my pension and then last year in excess of 100k which has caused the problems. Other issues surround how to pay. If you pay up front and the govt changes the rules in 18 months you�ve just spanked a lot of money. But if you go down the scheme pays route and they treat it as a loan - I believe that is how it works for the NHS Scheme Pays rules - you end up paying interest on the loan, a loan which you�ve never actually had the benefit from.

Its a mess, and it will get worse if we all go back to 75 Scheme in a few years and we get another lump sum thrown at pensions as reparation. But hey, numbers are boyuant, morale�s good and the PVR rate tiny. What�s to worry about?!

Vin Rouge

Your posts on this thread echo my thoughts ref AFPS.

It's possible as a Pilot, to earn large sums outside the mob, that enable you to put a significant amount of money into a workplace pension/SIPP that IMHO can rival the AFPS. I'm not saying AFPS is a bad scheme, but with the current job market It's possible to earn large sums outside the mob.

A "Gash Shag" airline Captain starting salary is circa 125K all in (that's from a good mate - ex Mil aged 40, now decent LoCo Captain who left 3.5 years ago and has just got Captaincy). The Military Flt Lt equivalent will be on less than 80K. He will most likely be a QFI/QWI etc etc etc. An airline equivalent (LTC/TRI/TRE) will be on more than the 125K above. He will also get paid extra for any other additional duties.

Now hypothetically speaking…..

The airline Captain has company pension contributions of 10% (so 12.5K). He chooses to max out his 40K annual allowance and contributes 27.5K (don't forget pension tax relief). His taxable salary is then just under 100K which makes sound financial sense keeping his taxable salary below 100K for income tax purposes. The difference in PAS vs airline salary after contributions is circa 20K - which can be spent as he sees fit.

I've not included contributions as an FO. Equally, I've used 20 years of contributions to keep things simple. Someone leaving age 40 could potentially work for up to 25 years. Again, I've also not included greater contributions (albeit with a tax hit) as a TRI/TRE etc.

20 years of contributions in this example gives an 800K pension pot. This will be in workplace pensions/a SIPP which provides diversification and flexibility that AFPS does not give.

Apologies for a long post. What I was going to ask is does anyone know how to work out how the AFPS contributions made on my behalf compare to my lifetime limit? I just went off on a bit of a tangent....

If anyone sees any flaw's with my calculations... then please shout!

Your posts on this thread echo my thoughts ref AFPS.

It's possible as a Pilot, to earn large sums outside the mob, that enable you to put a significant amount of money into a workplace pension/SIPP that IMHO can rival the AFPS. I'm not saying AFPS is a bad scheme, but with the current job market It's possible to earn large sums outside the mob.

A "Gash Shag" airline Captain starting salary is circa 125K all in (that's from a good mate - ex Mil aged 40, now decent LoCo Captain who left 3.5 years ago and has just got Captaincy). The Military Flt Lt equivalent will be on less than 80K. He will most likely be a QFI/QWI etc etc etc. An airline equivalent (LTC/TRI/TRE) will be on more than the 125K above. He will also get paid extra for any other additional duties.

Now hypothetically speaking…..

The airline Captain has company pension contributions of 10% (so 12.5K). He chooses to max out his 40K annual allowance and contributes 27.5K (don't forget pension tax relief). His taxable salary is then just under 100K which makes sound financial sense keeping his taxable salary below 100K for income tax purposes. The difference in PAS vs airline salary after contributions is circa 20K - which can be spent as he sees fit.

I've not included contributions as an FO. Equally, I've used 20 years of contributions to keep things simple. Someone leaving age 40 could potentially work for up to 25 years. Again, I've also not included greater contributions (albeit with a tax hit) as a TRI/TRE etc.

20 years of contributions in this example gives an 800K pension pot. This will be in workplace pensions/a SIPP which provides diversification and flexibility that AFPS does not give.

Apologies for a long post. What I was going to ask is does anyone know how to work out how the AFPS contributions made on my behalf compare to my lifetime limit? I just went off on a bit of a tangent....

If anyone sees any flaw's with my calculations... then please shout!

Last edited by Professor Plum; 12th Oct 2019 at 10:51.

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

Prof Plum, plus an additional point. 20k+ pay rise from the day you leave (including the pension you won�t get if you stay in) and a salary that won�t top out at Pay Point 30 on PA. Which barely matches the salary you start on as an FO from day one of leaving. The ability to deleverage earlier on in your career, through downpayment of the mortgage and overall quality of life increase from better salary also needs to be accounted for. No point enjoying a decent income at 90 with pea soup dribbling down my toothless grin.

Join Date: Aug 2009

Location: Odiham

Posts: 170

Likes: 0

Received 0 Likes

on

0 Posts

Medic view

I nearly got caught in this but was of an age that I could retire and return. The calculation is so complex that you almost need someone with a degree in maths to understand. One year, the calculation showed that I had contributed more than I had earned. I had applied and obtain a discretionary point for providing a service above my basic work. I also moved one step up the salary scale. The contribution into the pension involves something like the difference between last years salary and this year multiplied by 16. This is then added to your own and employers pension contributions. You then pay tax on the pension contribution above �40k. The things that have also caught people especially medics is taper rules. Your salary before tax including your pension contributions plus your employers pension contributions is your total rewards package. Once this goes above �110K (I think) then the amount you can contribute into your pension tapers from �40K. If you are lucky enough to have a total rewards package above �210K then the max you can put into a pension is �10K and you get taxed on contributions above these figures (55%) The problem is that you do not find out the contribution until October of the following tax year! A good IFA is vital.

This is why the NHS is in a mess and needs expensive locums (as reported in the papers today). The vast majority of my Consultant colleagues do not do extra paid work and are asking to reduce the hours they work

This is why the NHS is in a mess and needs expensive locums (as reported in the papers today). The vast majority of my Consultant colleagues do not do extra paid work and are asking to reduce the hours they work

Professor Plum

I think you are asking what pension contributions you would need to make to get a similar work-place pension? If so, the Govt Actuaries Dept (GAD) believe that to be 63.5% of your basic Service pay. If you were asking how much you have notionally paid in for Life Time Allowance (LTA) then Service personnel get an annual statement with that on these days. However, if you have left then you could ask Equinity, who took over from HM Paymaster some years back, and they can tell you what your LTA amount is.

The one flaw I would pick in your calcs for the comparison is that at 63.5% of your basic pay, then the PAS Flt Lt on say �70k per year is actually getting a �package� of ~�114.5k - as 63.5% of basic pay is ~�44.5k which is your notional pension contribution. Most Flt Lts that transfer to PAS at their 20/40 point, with the new RRP(F) in payment, will transfer to PAS Level 22 which is �70.5k. They will then go up each year as Flt Lts until PAS Level 30 which is currently �80k, which with the same pension amounts adds up to �130.8k. Now that isn�t that far off the sorts of numbers you have been talking for airline salaries. Honestly, if people are leaving the Services solely for pay reasons, unless they are able to take home more than �120-�150k a year, then they are really not thinking it through in my humble opinion. We haven�t even got to the other bits of the Armed Forces� package yet either - cheap SFA, CEA education allowance, Home to Duty, free medical and dental, separation allowance, etc...etc...

Now if you want to sell your soul and live in the Middle East in a compound for a few years to get �200k+ per annum, then that is a totally different ball game. But they pay you that much for a reason!

What I was going to ask is does anyone know how to work out how the AFPS contributions made on my behalf compare to my lifetime limit? I just went off on a bit of a tangent....

The one flaw I would pick in your calcs for the comparison is that at 63.5% of your basic pay, then the PAS Flt Lt on say �70k per year is actually getting a �package� of ~�114.5k - as 63.5% of basic pay is ~�44.5k which is your notional pension contribution. Most Flt Lts that transfer to PAS at their 20/40 point, with the new RRP(F) in payment, will transfer to PAS Level 22 which is �70.5k. They will then go up each year as Flt Lts until PAS Level 30 which is currently �80k, which with the same pension amounts adds up to �130.8k. Now that isn�t that far off the sorts of numbers you have been talking for airline salaries. Honestly, if people are leaving the Services solely for pay reasons, unless they are able to take home more than �120-�150k a year, then they are really not thinking it through in my humble opinion. We haven�t even got to the other bits of the Armed Forces� package yet either - cheap SFA, CEA education allowance, Home to Duty, free medical and dental, separation allowance, etc...etc...

Now if you want to sell your soul and live in the Middle East in a compound for a few years to get �200k+ per annum, then that is a totally different ball game. But they pay you that much for a reason!

VinRouge

Agreed, but you can leave at 55 with an EDP and have 25 years of reasonable health until it starts to go downhill a bit in your 80s. You don’t have to go full term to enjoy the benefits

No point enjoying a decent income at 90 with pea soup dribbling down my toothless grin.

Join Date: Sep 2003

Location: uk

Posts: 119

Likes: 0

Received 0 Likes

on

0 Posts

Professor Plum

I think you are asking what pension contributions you would need to make to get a similar work-place pension? If so, the Govt Actuaries Dept (GAD) believe that to be 63.5% of your basic Service pay. If you were asking how much you have notionally paid in for Life Time Allowance (LTA) then Service personnel get an annual statement with that on these days. However, if you have left then you could ask Equinity, who took over from HM Paymaster some years back, and they can tell you what your LTA amount is.

The one flaw I would pick in your calcs for the comparison is that at 63.5% of your basic pay, then the PAS Flt Lt on say �70k per year is actually getting a �package� of ~�114.5k - as 63.5% of basic pay is ~�44.5k which is your notional pension contribution. Most Flt Lts that transfer to PAS at their 20/40 point, with the new RRP(F) in payment, will transfer to PAS Level 22 which is �70.5k. They will then go up each year as Flt Lts until PAS Level 30 which is currently �80k, which with the same pension amounts adds up to �130.8k. Now that isn�t that far off the sorts of numbers you have been talking for airline salaries. Honestly, if people are leaving the Services solely for pay reasons, unless they are able to take home more than �120-�150k a year, then they are really not thinking it through in my humble opinion. We haven�t even got to the other bits of the Armed Forces� package yet either - cheap SFA, CEA education allowance, Home to Duty, free medical and dental, separation allowance, etc...etc...

Now if you want to sell your soul and live in the Middle East in a compound for a few years to get �200k+ per annum, then that is a totally different ball game. But they pay you that much for a reason!

I think you are asking what pension contributions you would need to make to get a similar work-place pension? If so, the Govt Actuaries Dept (GAD) believe that to be 63.5% of your basic Service pay. If you were asking how much you have notionally paid in for Life Time Allowance (LTA) then Service personnel get an annual statement with that on these days. However, if you have left then you could ask Equinity, who took over from HM Paymaster some years back, and they can tell you what your LTA amount is.

The one flaw I would pick in your calcs for the comparison is that at 63.5% of your basic pay, then the PAS Flt Lt on say �70k per year is actually getting a �package� of ~�114.5k - as 63.5% of basic pay is ~�44.5k which is your notional pension contribution. Most Flt Lts that transfer to PAS at their 20/40 point, with the new RRP(F) in payment, will transfer to PAS Level 22 which is �70.5k. They will then go up each year as Flt Lts until PAS Level 30 which is currently �80k, which with the same pension amounts adds up to �130.8k. Now that isn�t that far off the sorts of numbers you have been talking for airline salaries. Honestly, if people are leaving the Services solely for pay reasons, unless they are able to take home more than �120-�150k a year, then they are really not thinking it through in my humble opinion. We haven�t even got to the other bits of the Armed Forces� package yet either - cheap SFA, CEA education allowance, Home to Duty, free medical and dental, separation allowance, etc...etc...

Now if you want to sell your soul and live in the Middle East in a compound for a few years to get �200k+ per annum, then that is a totally different ball game. But they pay you that much for a reason!

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

LJ,

Please can you explain the rather significant jump in pensions contribution, as a % of pay that seems to have happened in the past 12 months? Are people all of a sudden getting vastly larger payouts on retirement? Has the AFPS calculator lined everyone�s post 55 driveway in gold? Can we all now afford a yacht?

Or has there been a change in assumption that is cynically screwing current serving personnel and turning it into a de facto contributory scheme via the back door? The figures pushed out as recently as last year were around the 45% of salary mark. Latest quote from official stats is now over 70% for officers. So what has changed? Why do we now have wing commanders receiving over 100% of their pay into their (imaginary) AFPS pension pots?

Please can you explain the rather significant jump in pensions contribution, as a % of pay that seems to have happened in the past 12 months? Are people all of a sudden getting vastly larger payouts on retirement? Has the AFPS calculator lined everyone�s post 55 driveway in gold? Can we all now afford a yacht?

Or has there been a change in assumption that is cynically screwing current serving personnel and turning it into a de facto contributory scheme via the back door? The figures pushed out as recently as last year were around the 45% of salary mark. Latest quote from official stats is now over 70% for officers. So what has changed? Why do we now have wing commanders receiving over 100% of their pay into their (imaginary) AFPS pension pots?

Last edited by VinRouge; 13th Oct 2019 at 09:36.

Join Date: Sep 2003

Location: uk

Posts: 119

Likes: 0

Received 0 Likes

on

0 Posts

LJ,

Please can you explain the rather significant jump in actuarial pensions contribution, as a % of pay that seems to have happened in the past 12 months? Are people all of a sudden getting vastly larger payouts on retirement? Has the AFPS calculator lined everyone�s driveway in gold? Can we all now afford a Nic 55 yacht, name it Rio Grande and drink cocktails in the Caribbean on retirement?

or has there been a change in assumption that is cynically screwing current serving personnel and turning it into a de facto contributory scheme via the back door? The figures pushed out by manning as recently as last year were around the 45% mark. Latest quote from official stats is now over 70% for officers. So what has changed? Why do we now have wing commanders receiving over 100% of their pay into their (imaginary) AFPS pension pots?

Please can you explain the rather significant jump in actuarial pensions contribution, as a % of pay that seems to have happened in the past 12 months? Are people all of a sudden getting vastly larger payouts on retirement? Has the AFPS calculator lined everyone�s driveway in gold? Can we all now afford a Nic 55 yacht, name it Rio Grande and drink cocktails in the Caribbean on retirement?

or has there been a change in assumption that is cynically screwing current serving personnel and turning it into a de facto contributory scheme via the back door? The figures pushed out by manning as recently as last year were around the 45% mark. Latest quote from official stats is now over 70% for officers. So what has changed? Why do we now have wing commanders receiving over 100% of their pay into their (imaginary) AFPS pension pots?

VinRouge

I think I have an explanation for both. Firstly, the �pension pot� to which you refer. It isn�t really a �pot� as you have correctly pointed out, it�s more of an IOU from HM Treasury. The scheme is written into UK Law and as we have agreed the pension that you have earned cannot be changed (and as we have learned in the McCloud case it cannot be unreasonably enforced for change without the consent of the scheme member - so AFPS15 should have been an offer to transfer for existing members like it was for AFPS05). There are millions of Govt IOUs in circulation right now, not for pensions but for payments - the Pound Sterling bank note. Have a look at one, in itself worth nothing, but the magical words of �I PROMISE TO PAY THE BEARER THE SUM OF�. This promise is backed by the Bank of England (or regional variations) and is in effect the same as our pensions - the UK promises to pay us the amount we have earned under the scheme underwritten in UK Law. I can remember talking to a Financial Advisor in the Mess in the very early 90s when I was a Pilot Officer, asking him what the Armed Forces Pension was - his answer was one of the best non-contributory pensions you can have and unless the country goes totally �belly up� then they have to pay you (by �belly up� we are looking at a significant hostile takeover by communists or the country going totally bankrupt - both unlikely).

When it comes to the 63.5%, it will vary as it is trying to map AN EQUIVALENT PRIVATE PENSION to the Armed Forces Pension Schemes. So every few years the Government Actuary Department (GAD) value what our pension would cost using several stable private pension schemes (the usual suspects and not the high-risk ones). They then come to a figure of what that would cost the individual if they were to buy that pension as a percentage of your basic pensionable salary (ie. excluding RRP(F), HTD, LSA, etc...). That figure is published as the SCAPE rate and a link follows on the latest valuation done in Mar 19 that is good for the next few years. The last time it was done it, I think in 2016, it was 51.5%.

Here is a link to the latest valuation: https://assets.publishing.service.go...8_Feb_2019.pdf

So that�s it, it can be valued and seen as a �virtual pot�, but to challenge it you would have to find flaws in the GAD�s independent processes (good luck with that!) or just accept it is about right by running one of the many pension calculators for private pension schemes - that is what I did and decided it was about right.

I think I have an explanation for both. Firstly, the �pension pot� to which you refer. It isn�t really a �pot� as you have correctly pointed out, it�s more of an IOU from HM Treasury. The scheme is written into UK Law and as we have agreed the pension that you have earned cannot be changed (and as we have learned in the McCloud case it cannot be unreasonably enforced for change without the consent of the scheme member - so AFPS15 should have been an offer to transfer for existing members like it was for AFPS05). There are millions of Govt IOUs in circulation right now, not for pensions but for payments - the Pound Sterling bank note. Have a look at one, in itself worth nothing, but the magical words of �I PROMISE TO PAY THE BEARER THE SUM OF�. This promise is backed by the Bank of England (or regional variations) and is in effect the same as our pensions - the UK promises to pay us the amount we have earned under the scheme underwritten in UK Law. I can remember talking to a Financial Advisor in the Mess in the very early 90s when I was a Pilot Officer, asking him what the Armed Forces Pension was - his answer was one of the best non-contributory pensions you can have and unless the country goes totally �belly up� then they have to pay you (by �belly up� we are looking at a significant hostile takeover by communists or the country going totally bankrupt - both unlikely).

When it comes to the 63.5%, it will vary as it is trying to map AN EQUIVALENT PRIVATE PENSION to the Armed Forces Pension Schemes. So every few years the Government Actuary Department (GAD) value what our pension would cost using several stable private pension schemes (the usual suspects and not the high-risk ones). They then come to a figure of what that would cost the individual if they were to buy that pension as a percentage of your basic pensionable salary (ie. excluding RRP(F), HTD, LSA, etc...). That figure is published as the SCAPE rate and a link follows on the latest valuation done in Mar 19 that is good for the next few years. The last time it was done it, I think in 2016, it was 51.5%.

Here is a link to the latest valuation: https://assets.publishing.service.go...8_Feb_2019.pdf

So that�s it, it can be valued and seen as a �virtual pot�, but to challenge it you would have to find flaws in the GAD�s independent processes (good luck with that!) or just accept it is about right by running one of the many pension calculators for private pension schemes - that is what I did and decided it was about right.

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

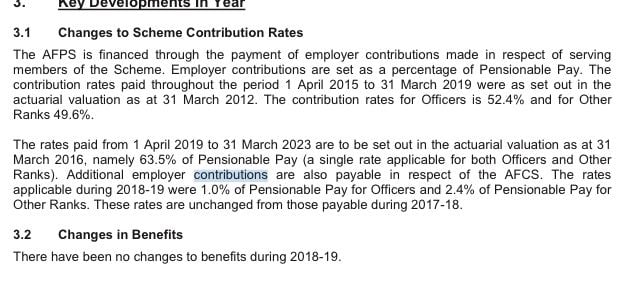

The GAD increased the contributions figure in 2016 for officers from 52.4% up to 63.5%. That is a pretty hefty increase mindful of the nil change to benefits.

some background here.

https://commonslibrary.parliament.uk...less-for-more/

I hope that makes sense? It�s a complex area that I haven�t got my head fully around as I have never had a bill (although I must be close!).

The GAD increased the contributions figure in 2016 for officers from 52.4% up to 63.5%. That is a pretty hefty increase mindful of the nil change to benefits.

some background here.

https://commonslibrary.parliament.uk...less-for-more/

Join Date: Jul 2007

Location: Germany

Posts: 1

Likes: 0

Received 0 Likes

on

0 Posts

You�re missing the point VinRouge . It is not about what the pension will pay you, it is what the pension will COST YOU. So if the private pension market performance is poor (which it is), then the valuation of what the AFPS would cost the Service person will increase. It�s not about what it pays you, it�s about what it would cost you.

risk etc. I know most who have hit but not exceeded annual limits and with the flexibility of their own provision and taking advice, have done far, far better than the �average�, which is a pretty poor use of your money. Again, HMG increasingly seem to be able to set whatever contribution rate they like (with advice from GAD), it then becomes a pseudo income stream when the Personal Allowance is accounted for.

It�s a bit like comparing the NAFFI Spar price for Jaffa cakes compared to what you can get them for in Tesco. Except you don�t get a choice.

Last edited by VinRouge; 13th Oct 2019 at 10:41.