New 'Bonza' LCC launches middle 2022 with B737 MAX

I assume you mean the perfect regional jet like an EMB-145ER and run between major regional centers like Albury, Dubbo, PortMaquarie, Brisbane and Essendon and so on for low cost operation... Then give it a snazzy name like JetGo... You might be onto something... Why do I sense a disturbance in the force...Oh well must be outside of my goldfish memory of bad ideas.

I assume you mean the perfect regional jet like an EMB-145ER and run between major regional centers like Albury, Dubbo, PortMaquarie, Brisbane and Essendon and so on for low cost operation... Then give it a snazzy name like JetGo... You might be onto something... Why do I sense a disturbance in the force...Oh well must be outside of my goldfish memory of bad ideas.

So their website says that “they will be revealing the location of their head office” soon and it will be in regional Australia.

Is there any sign of anything tangible. Not just a website and press releases?

Is there any sign of anything tangible. Not just a website and press releases?

At the CAPA conference the BONZA spokesperson stated they will be generating a new leisure oriented market as opposed to taking share of the exisiting ones. Also at that conference there was a prediction that business travel will decline by about 30-40% and be slow to recover. Consequently, if the operators that focus on business travel lose 30-40% of their income what will be the strategy to make up for the shortfall? (place additional focus on personal travel or reduce capacity?)

spokesperson stated they will be generating a new leisure oriented market as opposed to taking share of the exisiting ones.

Tiger tried a similar philosophy. What it means is that Barry and Kath who usually take the caravan to the coast for a holiday twice a year may be tempted into spending $99 each (plus bags, plus food) to fly somewhere more exotic like the Gold Coast.

So okay, a “new market”. Mmmmmm and when AJ and JH see the report on their desk that the new up start start up is getting good loads they will simply go head to head with them. Nothing the ACCC can do about that. Bring on competition blah blah blah.

I really hope I am wrong because we need more choice not less but I do not see a bright future.

I�d actually like to see Bonza succeed; for a country so dependent on air travel, Australia is overdue for a true LCC.

Unfortunately I don�t think the required cost base can be achieved, and they�ll just accrue too much debt getting the blessing of CASA before they even turn a blade.

Unfortunately I don�t think the required cost base can be achieved, and they�ll just accrue too much debt getting the blessing of CASA before they even turn a blade.

True LCC- how cheap should flights be FFS! JQ sell them cheap and yes they charge for all the ancillary products because that’s how they make their money. Ppl want cheap airfares thinking $50 is to much to go ex SY to anywhere need to have have a look at themself. I hope Bonza don’t even get an AOC.

True LCC- how cheap should flights be FFS! JQ sell them cheap and yes they charge for all the ancillary products because that�s how they make their money. Ppl want cheap airfares thinking $50 is to much to go ex SY to anywhere need to have have a look at themself. I hope Bonza don�t even get an AOC.

Join Date: Oct 2013

Location: New Zealand

Age: 71

Posts: 1,475

Likes: 0

Received 0 Likes

on

0 Posts

At the CAPA conference the BONZA spokesperson stated they will be generating a new leisure oriented market as opposed to taking share of the exisiting ones. Also at that conference there was a prediction that business travel will decline by about 30-40% and be slow to recover. Consequently, if the operators that focus on business travel lose 30-40% of their income what will be the strategy to make up for the shortfall?

Regarding fuel prices, here is a quote from an article on 5/1 in The Atlantic:�

The world has started to reduce its investment in producing fossil fuels. Right now, the world�s investment in oil and gas supply looks to be, somewhat shockingly, on track with a pathway of 1.5 degrees Celsius of global warming, according to the International Energy Agency. At the same time, the world is investing as much as ever in cars, power plants, and other products that use fossil fuels. That is, our investment in oil and gas demand still assumes a more-than-1.5-degree pathway. Consumers, companies, and countries seem to be assuming that oil and gas will be just as plentiful in the future as they are now.

The technical way to say this is that there is a mismatch between future oil supply expectations and future oil demand expectations. Let�s call this Mismatch No. 1.

The other mismatch is between clean energy and fossil fuels. Even as the world ramps down its investment in fossil-fuel supply, it isn�t investing enough in zero-carbon energy. According to the IEA, annual investment in clean-energy supply must triple for humanity to reach net zero by 2050. That�s Mismatch No. 2: The world is preparing for a net-zero world on the fossil-fuel side, but not on the clean-energy side.

Put together, these mismatches suggest that, if nothing changes, we can expect energy costs to go up. In the medium term, companies and consumers are going to want more oil and gas than the market can reasonably provide, and the price of both will increase.�

*

The world has started to reduce its investment in producing fossil fuels. Right now, the world�s investment in oil and gas supply looks to be, somewhat shockingly, on track with a pathway of 1.5 degrees Celsius of global warming, according to the International Energy Agency. At the same time, the world is investing as much as ever in cars, power plants, and other products that use fossil fuels. That is, our investment in oil and gas demand still assumes a more-than-1.5-degree pathway. Consumers, companies, and countries seem to be assuming that oil and gas will be just as plentiful in the future as they are now.

The technical way to say this is that there is a mismatch between future oil supply expectations and future oil demand expectations. Let�s call this Mismatch No. 1.

The other mismatch is between clean energy and fossil fuels. Even as the world ramps down its investment in fossil-fuel supply, it isn�t investing enough in zero-carbon energy. According to the IEA, annual investment in clean-energy supply must triple for humanity to reach net zero by 2050. That�s Mismatch No. 2: The world is preparing for a net-zero world on the fossil-fuel side, but not on the clean-energy side.

Put together, these mismatches suggest that, if nothing changes, we can expect energy costs to go up. In the medium term, companies and consumers are going to want more oil and gas than the market can reasonably provide, and the price of both will increase.�

*

At the CAPA conference one of the presenters stated that the aircraft leasing companies experienced increased profitability during the Covid period. Does anyone have any evidence to support or refute that claim? If the leasing companies did experience an upswing in profits, how did that eventuate?

Additionally, another piece of fact or fiction I came across suggests that aircraft leasing companies own approximately 50% of airline operators. This was in the context of the driving influence behind the increasing demand for narrow body versus wide body airliners.

If you possess a sound knowledge on these matters, much appreciate if you would share.

Additionally, another piece of fact or fiction I came across suggests that aircraft leasing companies own approximately 50% of airline operators. This was in the context of the driving influence behind the increasing demand for narrow body versus wide body airliners.

If you possess a sound knowledge on these matters, much appreciate if you would share.

Regarding fuel prices, here is a quote from an article on 5/1 in The Atlantic:”

The world has started to reduce its investment in producing fossil fuels. Right now, the world’s investment in oil and gas supply looks to be, somewhat shockingly, on track with a pathway of 1.5 degrees Celsius of global warming, according to the International Energy Agency. At the same time, the world is investing as much as ever in cars, power plants, and other products that use fossil fuels. That is, our investment in oil and gas demand still assumes a more-than-1.5-degree pathway. Consumers, companies, and countries seem to be assuming that oil and gas will be just as plentiful in the future as they are now.

The technical way to say this is that there is a mismatch between future oil supply expectations and future oil demand expectations. Let’s call this Mismatch No. 1.

The other mismatch is between clean energy and fossil fuels. Even as the world ramps down its investment in fossil-fuel supply, it isn’t investing enough in zero-carbon energy. According to the IEA, annual investment in clean-energy supply must triple for humanity to reach net zero by 2050. That’s Mismatch No. 2: The world is preparing for a net-zero world on the fossil-fuel side, but not on the clean-energy side.

Put together, these mismatches suggest that, if nothing changes, we can expect energy costs to go up. In the medium term, companies and consumers are going to want more oil and gas than the market can reasonably provide, and the price of both will increase.”

*

The world has started to reduce its investment in producing fossil fuels. Right now, the world’s investment in oil and gas supply looks to be, somewhat shockingly, on track with a pathway of 1.5 degrees Celsius of global warming, according to the International Energy Agency. At the same time, the world is investing as much as ever in cars, power plants, and other products that use fossil fuels. That is, our investment in oil and gas demand still assumes a more-than-1.5-degree pathway. Consumers, companies, and countries seem to be assuming that oil and gas will be just as plentiful in the future as they are now.

The technical way to say this is that there is a mismatch between future oil supply expectations and future oil demand expectations. Let’s call this Mismatch No. 1.

The other mismatch is between clean energy and fossil fuels. Even as the world ramps down its investment in fossil-fuel supply, it isn’t investing enough in zero-carbon energy. According to the IEA, annual investment in clean-energy supply must triple for humanity to reach net zero by 2050. That’s Mismatch No. 2: The world is preparing for a net-zero world on the fossil-fuel side, but not on the clean-energy side.

Put together, these mismatches suggest that, if nothing changes, we can expect energy costs to go up. In the medium term, companies and consumers are going to want more oil and gas than the market can reasonably provide, and the price of both will increase.”

*

What does that mean for aviation and especially leisure travel markets? One thing, more cost and getting used to less expansion and no cheap fares, good luck to any new entrants into the industry now.

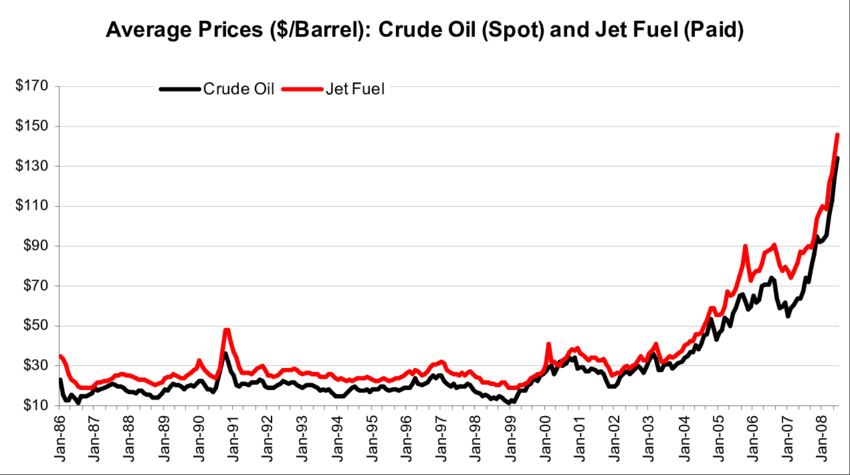

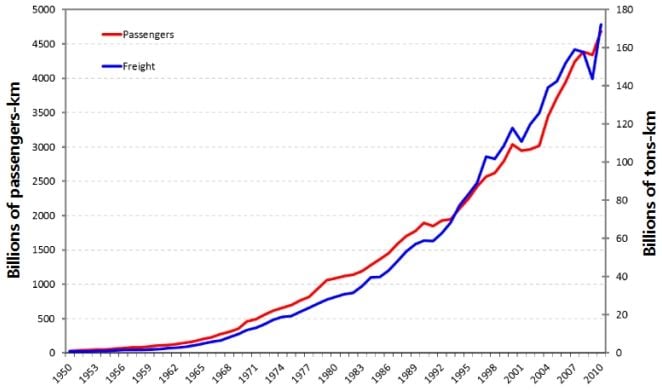

So a very quick search for data shows that despite a massive rise in the fuel price , there has been a massive rise in aviation activity over the last fifty years.

The sky is not falling. We are being manipulated…again.

This link shows that fuel is between 20-25% of operating costs depending on price, from IATA.

https://www.iata.org/contentassets/e...sheet-fuel.pdf

Flight numbers are definitely increasing, however how many airlines went broke during that period. There is a very aggressive approach to expansion in the airline industry that is not sustainable as once you hit the wall of profitable routes and have to make money on existing networks it all falls in a heap. This is all in the mantra of keeping airline travel and freight as cheap as possible to promote globalised supply chains and tourism dollars moving. Aviation will quickly over the coming years move to where trains and shipping have dwindled to, the pandemic will give airlines the helping hand to move things faster in that direction. It wasn't that long ago in the scheme of things that we had trains with segregated seating, 1st/2nd/3rd class coaches, ships and ferries the same, now its all one ticket on the cheapest possible platform. I'm not including the floating and railed theme parks like cruise ships and others that charge extra not to go anywhere in particular.

Aviation will quickly over the coming years move to where trains and shipping have dwindled to, the pandemic will give airlines the helping hand to move things faster in that direction.

It wasn't that long ago in the scheme of things that we had trains with segregated seating, 1st/2nd/3rd class coaches, ships and ferries the same, now its all one ticket on the cheapest possible platform.

https://www.eurail.com/en/help/inter...-and-2nd-class

https://www.japan-guide.com/e/e2016.html

https://www.amtrak.com/guide-to-fares

That was a slip, I meant general train and ferry travel. Not long distance travel such as city pairs. The dwindling was in reference to what is offered on such trips and accommodation, not that the service numbers themselves are dwindling. I traveled in Europe many years back, when they still had compartmented carriages and service staff, now that only applies to 1st class, which is a poor reflection of what 1st class used to be on trains. 1st class back not long ago was your own cabin, now its just a bigger seat, there are still sleepers though. Travel on local routes is vastly different to the high speed intercity routes also. Used to be commuter trains had the option of 1st to 3rd class seating. Deutsche Bahn operations are a bit hard to compare, as they are primarily government owned, we are not talking private companies here competing with each other.

Also important to note Amtrak is subsidised to the tune of $1.5billion USD, because no private company could provide sustainable intercity rail travel.

Also important to note Amtrak is subsidised to the tune of $1.5billion USD, because no private company could provide sustainable intercity rail travel.

At the CAPA conference one of the presenters stated that the aircraft leasing companies experienced increased profitability during the Covid period. Does anyone have any evidence to support or refute that claim? If the leasing companies did experience an upswing in profits, how did that eventuate?

Additionally, another piece of fact or fiction I came across suggests that aircraft leasing companies own approximately 50% of airline operators. This was in the context of the driving influence behind the increasing demand for narrow body versus wide body airliners.

If you possess a sound knowledge on these matters, much appreciate if you would share.

Additionally, another piece of fact or fiction I came across suggests that aircraft leasing companies own approximately 50% of airline operators. This was in the context of the driving influence behind the increasing demand for narrow body versus wide body airliners.

If you possess a sound knowledge on these matters, much appreciate if you would share.

As for the 50% of airline operators, I think what you may be thinking of is 50% of the in-service fleet of aircraft, which is about correct. Pre-pandemic it was between 43-48%, depending whose metric you looked at. Now I think the consensus is that it is just over 50% as more airlines moved to sale-and-leaseback financing to boost their liquidity. With most reserve banks printing money and sending interest rates to 0%, there has been a lot of cash looking for homes, and aircraft are one of the destinations that cash has ended up.