VA pilots worried about employment 2021

The going-concern value is often greater than the liquidation value of airlines, thereby motivating an infusion of capital into bankrupt or near bankruptcy airlines rather than their liquidation. Virgin isn't there yet. It has positive cash flow, has over a billion in cash reserves and it can service its debts.

can they issue more shares.. nope. They would need to be issued at a discount. Nobody will want to subscribe. Issue more corporate bonds.. I am sure those that bought the last lot and have lost 20% will be lining up to repeat the process.

as for positive cashflow.. nope.

Year end Dec 2019. Dec 2018

cash flow from operations. +$199m +$263m. Difference was restructuring costs of -62.4 in 2019

cash flow from investing. -$122.7m. -$263.6m. Difference was +131.8 disposal of assets in 2019

cash flow from financing. -$708.5m. -$198.7m

net cashflow. -632.1m. -199.3m

$200m positive from operations is easily wiped out by something like a virus.. but overall substantially negative cash flows in the last two non virus years.

I�m no finance man but I see they have a $350m usd bond due October next year. I assume a 100-150m loss this half. With the next FY only a quarter away, another 100m loss the back half this year.

So they will need another cash injection late next year?

So they will need another cash injection late next year?

Join Date: Aug 2007

Location: rice bowl

Posts: 113

Likes: 0

Received 0 Likes

on

0 Posts

Sounds familiar.

Mr. Twomey was banging on that Ansett had a billion dollars in the bank two weeks before Ansett collapsed. Only trouble, they owed four billion. Then the creditors called in the administrators. The Virgin rhetoric has been heard and used before.

Also Ansett had a lot of assets as reflected by over 90% of redundancies being delivered.

Mr. Twomey was banging on that Ansett had a billion dollars in the bank two weeks before Ansett collapsed. Only trouble, they owed four billion. Then the creditors called in the administrators. The Virgin rhetoric has been heard and used before.

Also Ansett had a lot of assets as reflected by over 90% of redundancies being delivered.

The little Italian guy told me himself. They were happy to contain the ongoing losses from the 777 at 1million a month. They didn't expect it to mprove due to factors like the dearest 777 leases in the world . He said they were keeping them for the code share opportunities . They were putting as many people on other operators and taking the profit. Sorry if you don't believe it. I've heard guys on the 330 claiming they were making money too.

Having a look at some A330 leasing rates you can see why he is so vocal in terms of its financial inefficiency. At the time Virgin signed the contract they were at an absolute premium of $1m a month. They now go for 30% less. It was obviously nothing more than a pissing contest at the time.

787-9 is cheaper to lease also. So 6x787s they could essentially lease for a lot less dollars compared to what they lease the current 330 fleet for. Plus bank the savings in fuel and loading efficiency.

Plus they can sell off the 777 fleet for what 100m a pop. 1x787 for Haneda and 5 to maintain LA.

That�s a lot of cost they will pull out.

They own 4/5 Triples and they are long paid off.

787-9 is cheaper to lease also. So 6x787s they could essentially lease for a lot less dollars compared to what they lease the current 330 fleet for. Plus bank the savings in fuel and loading efficiency.

Plus they can sell off the 777 fleet for what 100m a pop. 1x787 for Haneda and 5 to maintain LA.

That�s a lot of cost they will pull out.

They didn't expect it to mprove due to factors like the dearest 777 leases in the world

PoppaJoe: VA may not see October next year !. Your question "So they will need another cash injection late next year?" is best answered by saying they need to sell assets or find cash somewhere very soon. The Bonds sold in Nov 19 have lost 25% of their value. The current yield is 10.666%. Should the capital value fall lower ( I am of the opinion they will) with an increase in the yield they will be referred to as junk bonds.

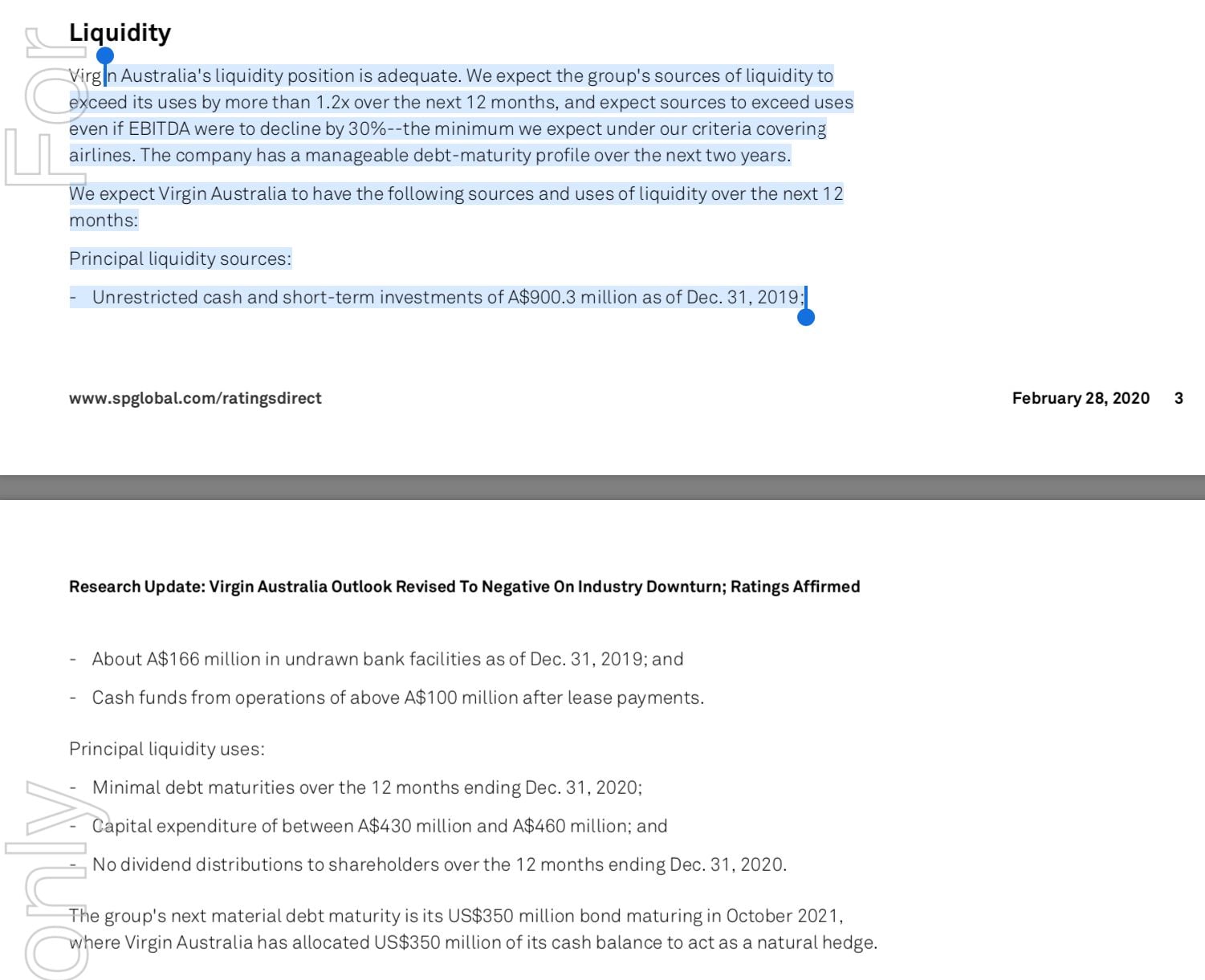

You may be aware on 28 Nov 2020 S&P Global Ratings revised its outlook on VA from stable to negative with B+ credit rating on the company. The companies debt is rated as B. The both of these ratings suggest VA is risky with a higher than average chance of default.

You may be aware on 28 Nov 2020 S&P Global Ratings revised its outlook on VA from stable to negative with B+ credit rating on the company. The companies debt is rated as B. The both of these ratings suggest VA is risky with a higher than average chance of default.

Join Date: Jan 2014

Location: Adelaide

Posts: 106

Likes: 0

Received 0 Likes

on

0 Posts

It made a massive mistake with its re positioning and re branding. Hundreds of millions of dollars down the drain and many years lost. Can it be turned around?

It has survived on the goodwill of its shareholders.

You know, you guys must be right. The 777 makes bucketloads. Let's change the name of this thread from "VA pilots worried about employment 2021" to something like " Cashed up VA announces big new widebody order". Oh

and happy international women's day, I'm sure they celebrated that with virgin flair...

and happy international women's day, I'm sure they celebrated that with virgin flair...

Last edited by The Baron; 7th Mar 2020 at 12:33.

Join Date: Aug 2009

Posts: 509

Likes: 0

Received 0 Likes

on

0 Posts

$200m positive from operations is easily wiped out by something like a virus.. but overall substantially negative cash flows in the last two non virus years.

So there are a couple of issues here. Firstly - what I was supposed to say was 'free cash flow', not 'positive cash flow'. My error. Second - looking at half-year results is 'half the picture'. It is a 'pulse check'. It's not an effective assessment. A lot can happen between halves that can drive performance up or down. You need to look at the full-year outcome. Thirdly - you need to consider both 'cash flow' and 'free cash flow'. They're different. Free cash flow is one of the most important measure of economic performance. It is a measure of the amount of cash flows that are truly unencumbered by the operation of the business. It is the purest measure of cash and forms the basis for valuation by removing the distorting effects of noncash charges, accounts for changes in working capital and acknowledges the capital expenditure for growth and have been avoided so far. It isolates the cash that is truly free to be distributed or used however VA sees fit.

For FY19 VA delivered 'positive free cash flow' of $53.9m. They raised the cash balance by $324m mostly through refinancing. And whilst it is also important to have 'positive cash flow' (not to be confused with free cash flow), you can see there is some large capital spending ($486.9m) in FY19 (and a lot of debt taken on under 'borrowings').

And we know in 1H20 they raised ~$1b via unsecured notes to fund a US$400m Bond that had expired (using debt to pay for debt) and to pay for Velocity ($700m). And they have dipped into cash reserves since that now reflects a reduction of $1.7b to $1.1b ($632m).

Don't get me wrong. Their debt levels are outrageous. Their leverage ratio is outrageous. They are dancing a debt tightrope and with cash flow reducing - they're ability to sustain will become challenged without spending all the reserves, selling off stuff, or raising more debt in the market (they can still do more of this - it just comes at a much higher price). And yes - their current liabilities are $1.5b greater than their assets. So if they were to collapse - there isn't going to be enough money to pay everyone (at this stage).

I see they have a $350m usd bond due October next year.

They'll likely refinance that or use a combination of cash and finance. All depends on the environment at that time.

And on B772's comments regarding their ratings - these are still opinions and need to be considered as that. Yes it does have an impact, but Qantas has been rated as 'junk' many times in the past.

Fingers crossed VA can continue to service debt for now. They may need to start a fire sale via Pickels Auctions... I see the airforce is selling some PC-9's there at the moment...

Join Date: Oct 2013

Location: New Zealand

Age: 71

Posts: 1,475

Likes: 0

Received 0 Likes

on

0 Posts

Why the hell did they bring back Keith Neate? He is one of the Godfrey gang who was part of the Executive idiot group between around 2003 - 2011 when countless colossal mistakes were made. He took a parachute over to Aurizon and Scurrah has brought him back. What a joke. Who will they bring back next - the king of fuel hedging cockups, Manny Gill? The airline has $5.4 billion in debt and excess of $1 billion of cash on its balance sheet and they have minimal assets. Anyone who thinks the $1b in cash will be their saviour needs their head read. As has been pointed out already, during a severe financial crisis $1b won�t get you that far.

Well if they are paying that bond with Cash then the balance will be down to 400m. But that number will be even lower once the next three half�s pass. Essentially it could be 100-200m left.

It looks like the MAX deal is largely split 50/50 lease/own also.

More cash needed!

Just get SQ to buy off Etihad, Chinese and the public.

It looks like the MAX deal is largely split 50/50 lease/own also.

More cash needed!

Just get SQ to buy off Etihad, Chinese and the public.

Everybody should be aware the results released by VA on 26 Feb 20 were for the period ended 31 Dec 19. Likewise the S&P Global Ratings Outlook Update report issued on 28 Feb 20 was based on information released by VA on 26 Feb 20. S&P then factor in what they believe has taken place since 01 Jan 20 and what they see in the future.

Since the release of the S&P Update the outlook has become bleaker due to concerns about Covid-19 and the impact on travel generally. The share price has collapsed a further 17.14% and what happens between now and 30 Jun 20 will determine the future of VA. S&P modelling up to 26 Feb 20 showed VA defaulting in 2024 unless their trajectory changes for the better. Should it worsen default could occur earlier. The S&P modelling suggested there could be just $311M available to cover estimated 'claims' of $2B in round figures.

Should market passenger numbers start to reduce this week and the VA market share fall even lower due to concerns by agents and the travelling public there are concerns about the viability of VA the outlook could change for the worse very quickly.

Since the release of the S&P Update the outlook has become bleaker due to concerns about Covid-19 and the impact on travel generally. The share price has collapsed a further 17.14% and what happens between now and 30 Jun 20 will determine the future of VA. S&P modelling up to 26 Feb 20 showed VA defaulting in 2024 unless their trajectory changes for the better. Should it worsen default could occur earlier. The S&P modelling suggested there could be just $311M available to cover estimated 'claims' of $2B in round figures.

Should market passenger numbers start to reduce this week and the VA market share fall even lower due to concerns by agents and the travelling public there are concerns about the viability of VA the outlook could change for the worse very quickly.

Last edited by B772; 7th Mar 2020 at 23:29.

Well if they are paying that bond with Cash then the balance will be down to 400m. But that number will be even lower once the next three half�s pass. Essentially it could be 100-200m left.

It looks like the MAX deal is largely split 50/50 lease/own also.

More cash needed!

Just get SQ to buy off Etihad, Chinese and the public.

It looks like the MAX deal is largely split 50/50 lease/own also.

More cash needed!

Just get SQ to buy off Etihad, Chinese and the public.

SQ have also booked losses from their VA investment in their own financial reports, and it's assumed that SQ are writing off their VA losses.

There's a better chance of VA's other partners: DL or NH taking over VA, and that's NOT likely to happen either.

Join Date: Feb 2018

Location: Hyperspace

Posts: 4

Likes: 0

Received 0 Likes

on

0 Posts

There is no ‘White Knight’ scenario here. All major shareholders are suffering their own pain.

All VA employees need to think seriously about the future.

I’ve said it before, this looks a LOT like another Ansett.

All VA employees need to think seriously about the future.

I’ve said it before, this looks a LOT like another Ansett.