So you need a new fleet Leigh?

Thread Starter

Join Date: Sep 2017

Location: Europe

Posts: 1,674

Likes: 0

Received 0 Likes

on

0 Posts

Airlines like Singapore and others have a small Low Fare Airline within the main game, no one else has a business the scale of JQ.

There is a reason why BA and Air New Zealand abandoned theirs.

It is not duplicated in scale or expanse in any other 'airline-within-an airline'.

Airlines like Singapore and others have a small Low Fare Airline within the main game, no one else has a business the scale of JQ.

There is a reason why BA and Air New Zealand abandoned theirs.

Airlines like Singapore and others have a small Low Fare Airline within the main game, no one else has a business the scale of JQ.

There is a reason why BA and Air New Zealand abandoned theirs.

Not having a domestic market does make it different however split it to longer international and domestic international distances.

Anyway back to the original thread...

QF 321NEO’s?

Project BananananaRamamaaa A350’???

OrnitalX...

Last edited by Global Aviator; 15th Jun 2019 at 02:31. Reason: Adding

Join Date: Aug 2009

Posts: 509

Likes: 0

Received 0 Likes

on

0 Posts

Jetstar's already saved Qantas. Where can its boss fly to next?

Started as a defence against Virgin, the budget airline is now a money making machine in its own right. So where to next for Jetstar and its man in charge?https://www.smh.com.au/business/comp...11-p51wnu.html

Join Date: May 2001

Location: Sydney

Age: 60

Posts: 1,542

Likes: 0

Received 0 Likes

on

0 Posts

Rebuking isn’t all that hard.

Even the commentators say it has cannibalised mainline, taking passengers that would have paid more and charging them less for their seats.

Even the commentators say it has cannibalised mainline, taking passengers that would have paid more and charging them less for their seats.

Ah of course.

Qantas Domestic repeatedly outperformed Jetstar, (As did Frequent Flyer), but Jetstar ‘saved’ Qantas. Bah! Yield, who needs it?!

JQ has its place, but come on now.

Though Perhaps Since JQ is such a money spinner the JQ pilots might like to remind their management of the vastly improved new Tiger Agreement (Tiger not as profitable). The ‘amazing’ business has been practically printing money and saving the entire group so they can obviously now afford to match it?!

Qantas Domestic repeatedly outperformed Jetstar, (As did Frequent Flyer), but Jetstar ‘saved’ Qantas. Bah! Yield, who needs it?!

JQ has its place, but come on now.

Though Perhaps Since JQ is such a money spinner the JQ pilots might like to remind their management of the vastly improved new Tiger Agreement (Tiger not as profitable). The ‘amazing’ business has been practically printing money and saving the entire group so they can obviously now afford to match it?!

That’s why the JQ pilots have the best T&Cs...

Oh, and, thank you for keeping the group solvent!!

Oh, and, thank you for keeping the group solvent!!

Thread Starter

Join Date: Sep 2017

Location: Europe

Posts: 1,674

Likes: 0

Received 0 Likes

on

0 Posts

Assuming you asked with a genuine desire to understand how Jetstar is far from a saviour, it is worth remembering statements like Mr Evans are impossible to test. Mr Evans knows that. If Mr Evans wishes to open the company to scrutiny, invite investigation and stand behind such an assertion, then there are simple things he can do:

1. Segment Jetstar International as a separate operating segment.

After all the parent who needed saving is reported separately from FY12. (i.e. QF International and QF domestic) Presumably he is happy to do this to show the value add?

2. Detail precisely what rate Jetstar pays to Qantas for the A320, 787 and A321 aircraft.

Qantas retains ownership of the aircraft, ‘leasing’ them to Jetstar. It is highly probable from our figures that the rate is nowhere near a commercial rate, therefore it remains an effective subsidy which advantages Jetstar.

Inherently, Jetstar ought to meet the requirements of a reportable segment, probably ought exceed the qualitative and quantitative thresholds in AASB 8 Operating Segments. Even if they don't senior management can ‘choose’ to report a segment anyway if they believe doing so would be of benefit to investors. Ask yourself why they do not?

Whilst discounted leases are in no way illegal, they do hide an effective subsidy, which is material to any assertion made by Mr Evans and he knows this.

The Air Transport Licensing Authority (ATLA) decision regarding Jetstar Hong Kong detailed specifically that ownership and control of the aircraft resided with Qantas, not Jetstar Hong Kong.

This was a central tenet of the rejection of the application.

When Little Napoleon ascended the throne, Jetstar had a fleet less than 40, now their fleet (with their associates) is larger than the parent. Despite this scale and flying some 48% of the ASK of the parent they cannot generate more than 30% of the revenue. Total group revenue in the year before Little Napoleon's coronation was 12% higher in real terms than today. Qantas group, in a decade went backwards in real terms.

Let not actual facts get in the way of a good story.

Qantas need a new fleet.

1. Segment Jetstar International as a separate operating segment.

After all the parent who needed saving is reported separately from FY12. (i.e. QF International and QF domestic) Presumably he is happy to do this to show the value add?

2. Detail precisely what rate Jetstar pays to Qantas for the A320, 787 and A321 aircraft.

Qantas retains ownership of the aircraft, ‘leasing’ them to Jetstar. It is highly probable from our figures that the rate is nowhere near a commercial rate, therefore it remains an effective subsidy which advantages Jetstar.

Inherently, Jetstar ought to meet the requirements of a reportable segment, probably ought exceed the qualitative and quantitative thresholds in AASB 8 Operating Segments. Even if they don't senior management can ‘choose’ to report a segment anyway if they believe doing so would be of benefit to investors. Ask yourself why they do not?

Whilst discounted leases are in no way illegal, they do hide an effective subsidy, which is material to any assertion made by Mr Evans and he knows this.

The Air Transport Licensing Authority (ATLA) decision regarding Jetstar Hong Kong detailed specifically that ownership and control of the aircraft resided with Qantas, not Jetstar Hong Kong.

This was a central tenet of the rejection of the application.

When Little Napoleon ascended the throne, Jetstar had a fleet less than 40, now their fleet (with their associates) is larger than the parent. Despite this scale and flying some 48% of the ASK of the parent they cannot generate more than 30% of the revenue. Total group revenue in the year before Little Napoleon's coronation was 12% higher in real terms than today. Qantas group, in a decade went backwards in real terms.

Let not actual facts get in the way of a good story.

Qantas need a new fleet.

Last edited by Rated De; 15th Jun 2019 at 08:53. Reason: Readability.

Rated De,

And what is the point here ? What are you trying to say ?

Despite this scale and flying some 48% of the ASK of the parent they cannot generate more than 30% of the revenue

Last edited by a_pilot; 15th Jun 2019 at 10:20.

Thread Starter

Join Date: Sep 2017

Location: Europe

Posts: 1,674

Likes: 0

Received 0 Likes

on

0 Posts

An issue of scale.

If you look at the segment revenues, deploying an additional ASK (at the margin) to Qantas instead of Jetstar delivers more revenue.

In the absence 'like for like' cost apportionment (management deciding who pays for what) Qantas can claim that 'lower unit cost' means Jetstar has better operating margin.

Mr Evans admits that the unit cost at Jetstar is somewhere between an established and a low fare airline, stating,

Thus, as a mid cost airline its margins are narrow, particularly with respect to how little revenue it generates from flying its ASK.

It is highly probable that the parent picks up the cost of many things including the aircraft capital cost, some engineering and port costs. Be creative there is literally no limit!

Thus, it needs a new fleet to again lower its unit cost, a fact to which Mr Evans also alludes. Bruce Buchanan (former JQ CEO) lamented this problem during his tenure.

Comparing Qantas unit costs to competitor airlines shows Qantas mid way. Qantas enjoyed, until management trashed the brand a substantive yield premium for product.

The trick to remember is what the late CEO Herb Kelleher of Southwest said;

(paraphrasing)

"You can have the lowest cost airline, or the highest revenue airline and still go broke. What matters is the gap between the two."

If Little Napoleon has really 'transformed' Qantas it ought have a lower unit cost and better operating margin.

This operating margin would be orders of magnitude better if they had, like all their competitors, re-equipped the fleet with fuel efficient long range wide body twins.

Instead, they persist pouring capacity into Jetstar, in a forlorn attempt to grow. The may grow capacity, but the (revenue) return from the additional capacity indicates rather strongly that the growth in revenue is sub optimal.

A new fleet of Qantas International would have almost halved their CASK (fuel included).

If you look at the segment revenues, deploying an additional ASK (at the margin) to Qantas instead of Jetstar delivers more revenue.

In the absence 'like for like' cost apportionment (management deciding who pays for what) Qantas can claim that 'lower unit cost' means Jetstar has better operating margin.

Mr Evans admits that the unit cost at Jetstar is somewhere between an established and a low fare airline, stating,

Should it be like the much-derided Irish carrier Ryanair, which charges passengers Ł20 ($36) if they haven't printed their own boarding pass and Ł55 ($100) if they haven't checked in online?Or closer to a "hybrid" carrier, which impinge the on full-service market like JetBlue in the US or even Virgin Australia.

Evans says Jetstar has landed somewhere in the middle, because that's where its customers want it to be

Evans says Jetstar has landed somewhere in the middle, because that's where its customers want it to be

Thus, as a mid cost airline its margins are narrow, particularly with respect to how little revenue it generates from flying its ASK.

It is highly probable that the parent picks up the cost of many things including the aircraft capital cost, some engineering and port costs. Be creative there is literally no limit!

Thus, it needs a new fleet to again lower its unit cost, a fact to which Mr Evans also alludes. Bruce Buchanan (former JQ CEO) lamented this problem during his tenure.

Comparing Qantas unit costs to competitor airlines shows Qantas mid way. Qantas enjoyed, until management trashed the brand a substantive yield premium for product.

The trick to remember is what the late CEO Herb Kelleher of Southwest said;

(paraphrasing)

"You can have the lowest cost airline, or the highest revenue airline and still go broke. What matters is the gap between the two."

If Little Napoleon has really 'transformed' Qantas it ought have a lower unit cost and better operating margin.

This operating margin would be orders of magnitude better if they had, like all their competitors, re-equipped the fleet with fuel efficient long range wide body twins.

Instead, they persist pouring capacity into Jetstar, in a forlorn attempt to grow. The may grow capacity, but the (revenue) return from the additional capacity indicates rather strongly that the growth in revenue is sub optimal.

A new fleet of Qantas International would have almost halved their CASK (fuel included).

Rated De,

Just a simple basic question.

What is more important for a business, revenue or profit ?

What is essential for it to survive, revenue or profit ?

For the shareholders, are dividends based on revenue or profit ?

For the staff, is the bonus based on revenue or profit ?

Just a simple basic question.

What is more important for a business, revenue or profit ?

What is essential for it to survive, revenue or profit ?

For the shareholders, are dividends based on revenue or profit ?

For the staff, is the bonus based on revenue or profit ?

Last edited by a_pilot; 15th Jun 2019 at 13:17.

Join Date: Feb 2018

Location: Wellington

Posts: 258

Likes: 0

Received 0 Likes

on

0 Posts

So can someone explain to a simpleton like me..why are Joyce/ Evans and their hired help (Harbinson etc) talking it up- ie the Strategic basis of this- other than it's EA time.

Join Date: Jul 2014

Location: Harbour Master Place

Posts: 662

Likes: 0

Received 0 Likes

on

0 Posts

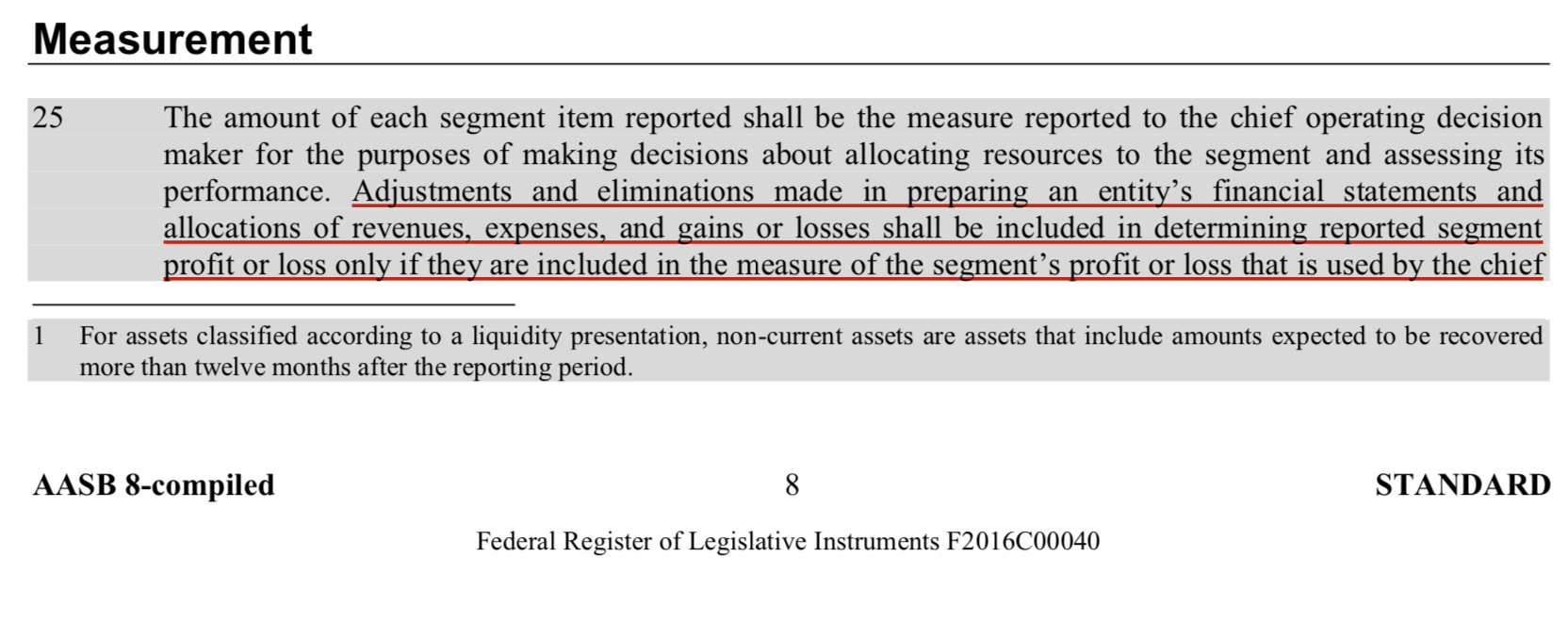

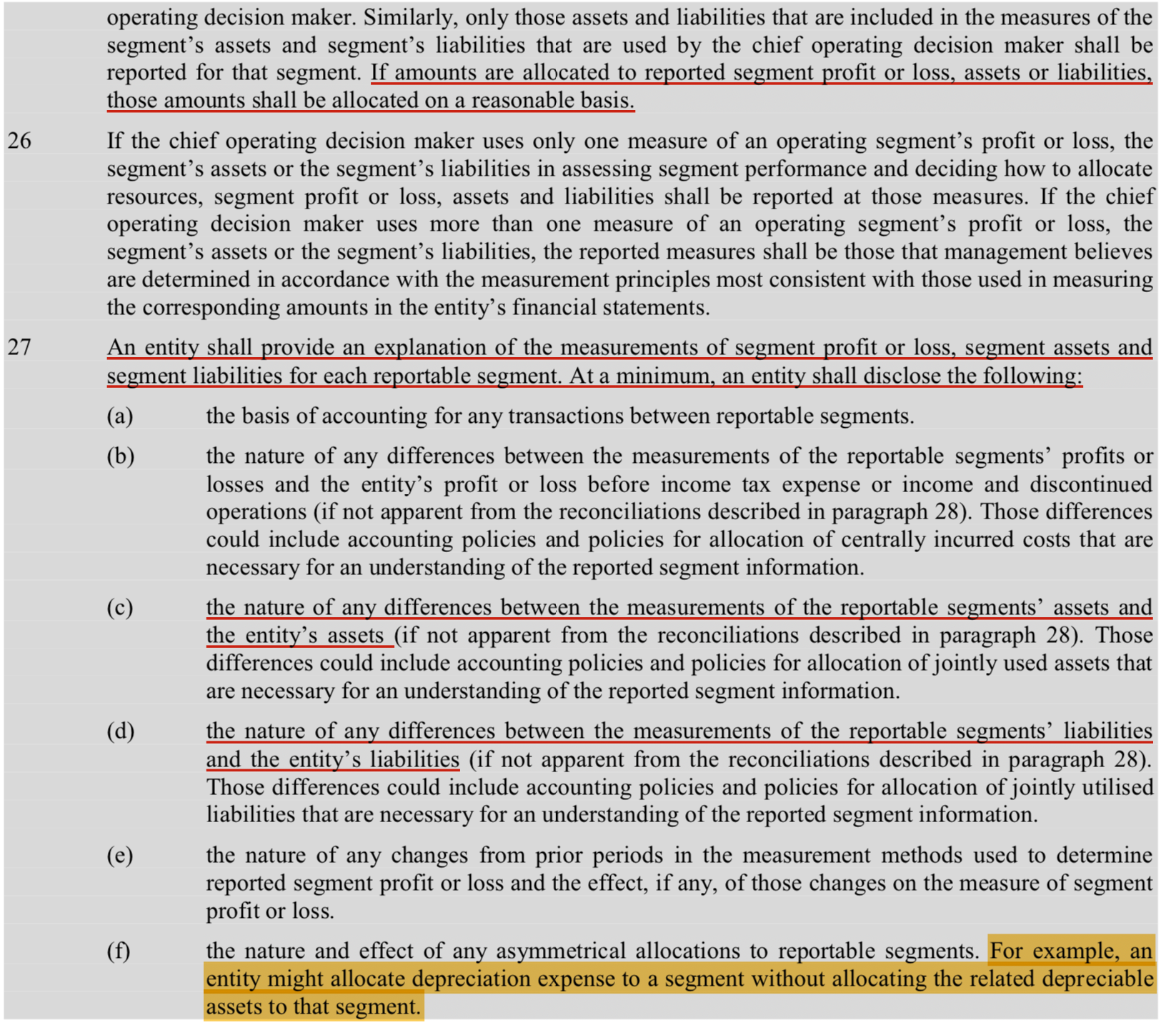

Read the Australian Accounting Standard on segment accounting. AASB8 and decide for yourself.

As an outsider, corporate accounting looks a bit like the responsibility of a Pilot In Command. Lots of general rules and principles, but ultimately a lot of flexibility to run the Corporation in a non-prescriptive (from a legal perspective) manner as the "Chief Operating Decision Maker" deems fit.

My interpretation of the rules is this: You have lots of flexibility to arrange your segments how you deem fit, and note how you did it in your segment accounts. However, those segment account notes are not required to be disclosed in the aggregated financial report. This subtle difference in reporting requirements is the crack that Qantas wedged open to drive the proverbial truck through for industrial relations purposes.

There is no contradiction between shifting revenues and costs between entities "on a reasonable basis", turning profitable internal entities into loss making ones and vice versa, and making public statements to that effect. Without the accounting report & notes and the basis of those shifts it is impossible to actually determine what really happens in each entity. Qantas could choose to report those internal segment accounts, however they don't. Therefore, public statements on the profitability of any internal entity is on a "trust us" on what is a "reasonable" basis.

But you don't need to take my word for it, read the standard yourself and draw your own conclusions.

As an outsider, corporate accounting looks a bit like the responsibility of a Pilot In Command. Lots of general rules and principles, but ultimately a lot of flexibility to run the Corporation in a non-prescriptive (from a legal perspective) manner as the "Chief Operating Decision Maker" deems fit.

My interpretation of the rules is this: You have lots of flexibility to arrange your segments how you deem fit, and note how you did it in your segment accounts. However, those segment account notes are not required to be disclosed in the aggregated financial report. This subtle difference in reporting requirements is the crack that Qantas wedged open to drive the proverbial truck through for industrial relations purposes.

There is no contradiction between shifting revenues and costs between entities "on a reasonable basis", turning profitable internal entities into loss making ones and vice versa, and making public statements to that effect. Without the accounting report & notes and the basis of those shifts it is impossible to actually determine what really happens in each entity. Qantas could choose to report those internal segment accounts, however they don't. Therefore, public statements on the profitability of any internal entity is on a "trust us" on what is a "reasonable" basis.

But you don't need to take my word for it, read the standard yourself and draw your own conclusions.

Join Date: Apr 2007

Location: earth

Posts: 78

Likes: 0

Received 0 Likes

on

0 Posts

And Rated is trying to illustrate that JQ's profits, if any, may be illusory.

Qantas retains ownership of the aircraft, ‘leasing’ them to Jetstar. It is highly probable from our figures that the rate is nowhere near a commercial rate, therefore it remains an effective subsidy which advantages Jetstar.

Could I suggest that Rated De is not doing a very good job at proving this ?

With no basis in fact, and without evidence, we are left to consider this view as opinion, or 'the vibe'.

Qantas retains ownership of the aircraft, ‘leasing’ them to Jetstar. It is highly probable from our figures that the rate is nowhere near a commercial rate, therefore it remains an effective subsidy which advantages Jetstar.

Could I suggest that Rated De is not doing a very good job at proving this ?

With no basis in fact, and without evidence, we are left to consider this view as opinion, or 'the vibe'.